August 17, 2011

In its fiscal year 2012 budget proposal, the Chicago Public Schools administration provided for the first time a three-year projection of its future financial situation on page 9. The projection shows that the total CPS employer pension contribution is expected to jump from $219.3 million in FY2013 to $671.7 million in FY2014, adding over $450 million in expenditure pressure to the CPS operating budget that year.

This spike is primarily the result of 2010 legislation that gave CPS a three-year partial reprieve from making its full employer pension contributions to the Chicago Teachers’ Pension Fund (CTPF). The 1995 law (Public Act 89-15) that put CPS under the control of the mayor of Chicago also changed the District’s pension funding requirements. It set the minimum CPS employer contribution to CTPF as an amount needed to bring the total assets of the Fund up to 90% of the total actuarial liabilities by the end of FY2045. This “90% funded in 50 years” structure is the same one that was adopted by the General Assembly for the five State of Illinois retirement systems.

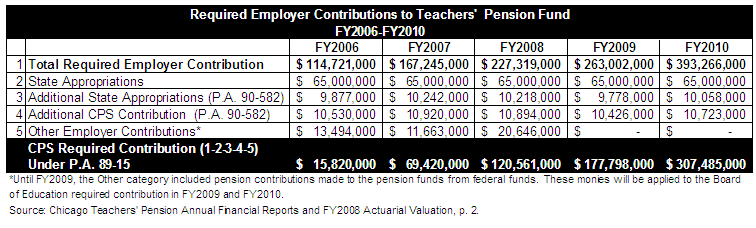

P.A. 89-15 did not require CPS to make an employer contribution on this schedule as long as CTPF was over 90% funded. After several years of funded ratios at or near 100%, the funded ratio dropped below 90% in FY2004, triggering CPS employer contributions per the statutory schedule beginning in FY2006 (the schedule also included a 15-year ramp up to the amount needed to reach 90% by 2045, as did the schedule for the five State retirement funds). By this time CPS had gone several years without making a substantial pension contribution and had to find room in its operating budget for this obligation. The CPS contribution required under P.A. 89-15 quickly grew from $15.8 million in FY2006 to $307.5 million in FY2010.

In March 2010, the FY2011 CPS required contribution under P.A. 89-15 was calculated to be $586.9 million, or almost double the FY2010 amount.[1] CPS had just announced an expected $900 million budget shortfall for FY2011. In April 2010, Public Act 96-0889 reduced pension benefits for many public employees hired on or after January 1, 2011 and reduced the CPS employer contributions required under P.A. 89-15 for FY2011, FY2012 and FY2013 to an amount estimated to be equivalent to the normal cost.[2] The District’s required FY2011 contribution declined to $187.0 million, which was $120.5 million or 39.2% less than the prior year contribution.[3] When the Act was signed in April 2010, it cut the District’s then-projected $1 billion FY2011 budget shortfall to $600 million.

P.A. 96-0889 also delayed the year that the pension fund must reach a 90% funded ratio from 2045 to 2059. Beginning with FY2014, the total required employer contribution will be calculated as a level percentage of payroll through FY2059. The CPS required contribution will be the total amount of the required employer contribution less additional state appropriations, additional CPS appropriations and other employer appropriations.

The exhibit below shows actuarial projections of required CPS contributions to the Teachers’ Pension Fund from FY2011 to FY2020 based on P.A. 96-0889. As noted above, the FY2011, FY2012 and FY2013 amounts were fixed in state statute but in FY2014 the required contribution will be actuarially determined as the schedule to reach 90% funded by the end of 2059 begins. The projected FY2014 contribution more than triples from the previous year, growing by $451.8 million from $196.0 million in FY2013 to $647.8 million in FY2014. The required employer contribution will be recalculated each year based on the status of the Fund.

In summary, CPS received a three-year reprieve on its required pension contributions, but this delayed the date when large contributions must be made. The delay will also exacerbate the deteriorating health of the pension fund, making future required contributions even higher.