August 31, 2011

Illinois’ Personal Property Replacement Tax (PPRT) is a revenue source for local governments that was created by the General Assembly in 1979 to replace a tax on the personal property of businesses that was abolished pursuant to the 1970 Illinois Constitution Article IX Section 5.

Although its name refers to the tax it replaces, the PPRT is an income tax on the federal taxable income of corporations, business partnerships, trusts and Subchapter S corporations and a tax on public utilities at the following rates:

Income Tax:

- corporations: 2.5% of federal taxable income

- partnerships, trusts and subchapter S corporations: 1.5% of federal taxable income

Invested Capital Tax:

- rural electric cooperatives and businesses that sell gas, electric or water service: 0.8% of capital invested in gas, electric and water facilities

Electricity Distribution Tax:

- electricity distributors (except rural electric cooperatives): ranges from 0.031 cents to 0.131 cents per kilowatt hour distributed, subject to overall annual limit

Telecommunications Infrastructure Maintenance Fee:

- telecommunications services: 0.5% of retailer’s gross charges for telecommunications services

Various exemptions and credits are also applied to PPRT.

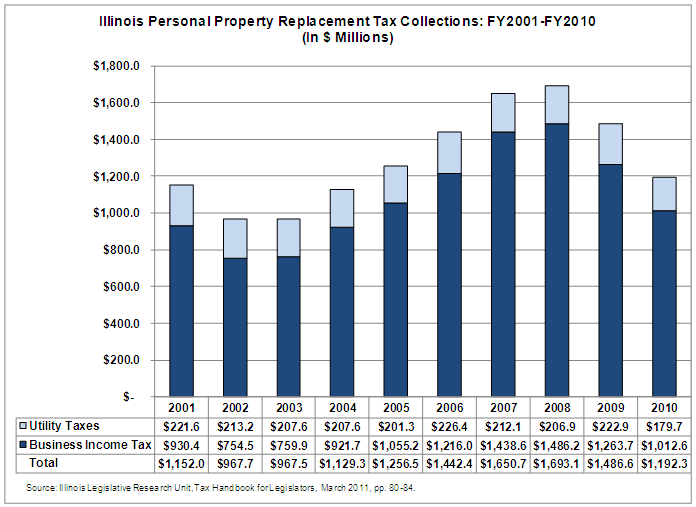

Total PPRT collections peaked in the State of Illinois’ Fiscal Year 2008 (year ending June 30, 2008) at $1.7 billion and by FY2010 had fallen below the FY2005 receipts. While the utility taxes portion of PPRT is somewhat less volatile than the business income tax portion, it only represents roughly 15% of annual PPRT revenues.

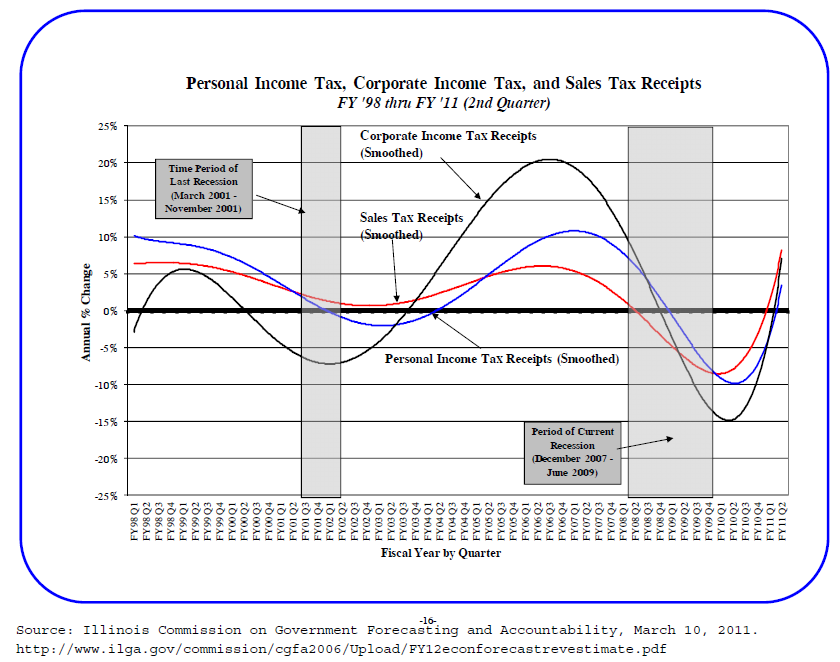

PPRT is an inherently volatile revenue source because business income tax receipts are so closely tied to economic cycles. The following graph produced by Illinois’ Commission on Government Forecasting and Accountability illustrates the relative volatility of sales taxes, personal income taxes and business income taxes. Business income taxes show the greatest increases and decreases.

Click here to download a PDF of the above chart.

PPRT revenues are affected by factors other than the business cycle, however. State tax amnesty programs and changes to refund rates can result in collections that do not directly reflect economic cycles. The amount of PPRT revenue distributed to local governments could also be affected by diversion of the revenue for other uses. For example, Public Act 97-0002 requires stipends and expenses for certain local government officials and the Property Tax Appeals Board to be paid out of PPRT collections before they are distributed to local governments and a similar proposal to pay regional superintendents of education may arise.

Net PPRT revenues are distributed to local governments in the following manner: 51.65% to Cook County governments based on shares of personal property tax collections in 1976, and 48.35% to local governments in the rest of the state based on personal property tax collections in 1977.

For many units of government PPRT represents less than 5% of annual revenues, but for some it represents much more. An analysis by the Chicago Metropolitan Agency for Planning found that PPRT provided over 10% of revenue for 39 out of 1,052 governments in a seven-county region of northeastern Illinois in 2010.

The volatility of PPRT and the fact that PPRT distributions can be affected by other State actions as described above make it a relatively unpredictable revenue source. Therefore, it is prudent for local governments not to rely on annual PPRT revenues as an operating budget revenue source. City Colleges of Chicago made the wise decision to direct PPRT revenues to its capital fund beginning in FY2011. As noted in the Civic Federation’s analysis of the City Colleges budget (page 4), pay-as-you-go capital programs can withstand greater volatility because projects can be postponed if revenues come in under budget. Operating budgets should be supported by predictable revenue sources in order to maintain stability. It is not prudent to dedicate unusually high revenues generated by economically sensitive sources during periods of economic expansion to ongoing programs that must be reduced or cut when the economy contracts.

The Civic Federation urges other local governments to adopt a similar practice and reduce reliance on PPRT revenues for operating purposes. A best practice would be to adopt a financial policy regarding volatile revenue sources. A government could adopt a policy not to use revenue from volatile sources that exceeds normal growth rates (defined as the average annual growth rate over the past ten years) for ongoing operating costs. Any additional revenue over the average amount would be dedicated to capital projects, fund balance or reducing long-term liabilities (including unfunded pension liabilities).