August 31, 2016

In 2012 the Governmental Accounting Standards Board (GASB) issued new accounting and financial reporting standards for public pension plans and for governments, Statements 67 and 68. According to GASB, the new standards were intended to “improve the way state and local governments report their pension liabilities and expenses, resulting in a more faithful representation of the full impact of these obligations.”[1]

Among other disclosures, pension funds and governments are now required to report total pension liability, fiduciary net position, net pension liability, pension expense and actuarially determined contribution (ADC), which are calculated on a different basis from previous GASB 25 and 27 pension disclosure requirements. Both pension funds and governments must also disclose additional information about pensions in the notes to the financial statements and in required supplementary information sections. It is important to note that GASB intended to separate pension reporting from pension funding. Thus, the numbers reported according to GASB 67 and 68 standards are not used to determine how much a government must contribute to its pensions. They are a reporting, NOT a funding requirement. Chicago Public Schools and other governments will continue to use traditional public pension accounting methods to determine funding requirements. However, as the GASB 67 and 68 numbers can provide important new ways to understand a fund’s sustainability, the Federation will address them here.

The Chicago Teachers’ Pension Fund (CTPF) began reporting according to GASB 67 in its FY2014 CAFR and actuarial valuations. The Chicago Public Schools began reporting according to GASB 68 in its FY2015 financial statements.

The total pension liability, fiduciary net position, net pension liability and ADC[2] are all calculated on a different basis both from what used to be required by GASB and from the traditional public pension actuarial basis.

Total Pension Liability – This number is similar in concept to the actuarial accrued liability (AAL), but is NOT the same. The actuarial cost method and discount rate (among other things) are different. All plans are required to use:

- Entry age normal actuarial cost method and level percent of payroll. CTPF uses projected unit credit, a different cost allocation method for statutory reporting and funding purposes.

- A single blended discount rate, instead of basing the discount rate only on projected investment earnings. The discount rate is used to calculate the present value of the future obligations of a pension fund. The discount rate has an inverse relationship to actuarial liabilities, such that a lower discount rate will result in higher liabilities.

- If a government is projected to have enough assets to cover its projected benefit payments to current and inactive employees, it can use the expected return on investments as its discount rate.

- If a government is projected to reach a crossover point beyond which projected assets are insufficient to cover projected benefit payments, then a blended discount rate must be used. Benefit payments projected to be made from that point forward are discounted using a high-quality municipal bond interest rate. The blended rate is a single equivalent rate that reflects the investment rate of return and the high-quality municipal bond interest rate.

- The Chicago Teachers’ Pension Fund was not projected to reach the crossover point, so its GASB 67 and 68 reporting is discounted at the full 7.75% assumed rate of return.

Fiduciary Net Position – This number is essentially the market value of assets in the pension plan as of the end of the fiscal year, not the assets as calculated on an actuarially smoothed basis under previous reporting requirements. CTPF still uses smoothed actuarial value of assets to determine statutory employer contribution requirements.

Net Pension Liability – This number is similar in concept to the unfunded actuarial accrued liability, but again is NOT the same. It is the difference between the Total Pension Liability and the Fiduciary Net Position of the fund. Governments are required to report the Net Pension Liability in their Statements of Net Position in their financial statements, according to GASB 68.

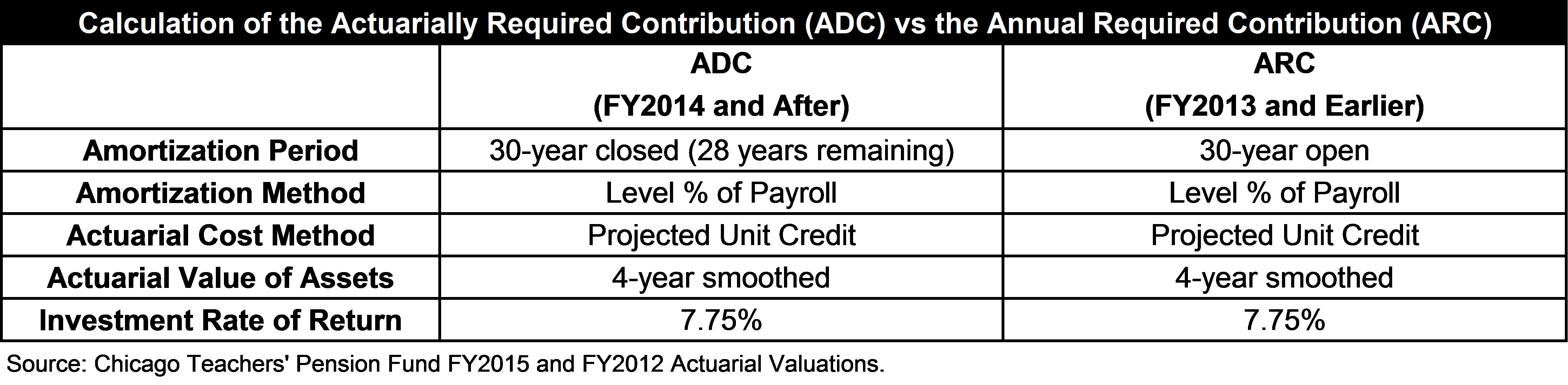

Actuarially Determined Contribution (ADC) – Another change from previous standards is that funds are no longer required to report an Annual Required Contribution (ARC) based on standards promulgated by GASB. Instead, the funds will calculate an Actuarially Determined Contribution or ADC that reflects their own funding plan, unless that funding scheme does not follow actuarial standards of practice. Then the fund must report an ADC that is calculated according to actuarial standards of practice. It is again important to emphasize that the ADC is a reporting and not a funding requirement. See the discussion below for a summary of how the basis for calculating the Teachers’ Fund ADC differs from the ARC.

Difference between the ADC and ARC

Depending on the employer’s funding plan, a pension fund’s ADC may be very similar to the previously reported ARC. The chart below summarizes the main assumptions behind the Chicago Teachers’ Pension Fund calculations of ADC and ARC. The only difference between the two numbers is that the ADC has a closed amortization period and the ARC had an open amortization period. An open amortization period remains the same every year (e.g., each valuation amortizes UAAL over 30 years), while a closed amortization period declines as each year passes (e.g., successive valuations amortize at 30 years, 29 years, 28 years, etc.). The ADC uses the actuarially calculated UAAL number instead of the GASB 67 net pension liability number, which also makes it similar to the ARC. Additionally, the ADC need not follow the GASB 67 and 68 requirement of using the market value of assets. The CTPF uses a four-year smoothed valuation of assets.

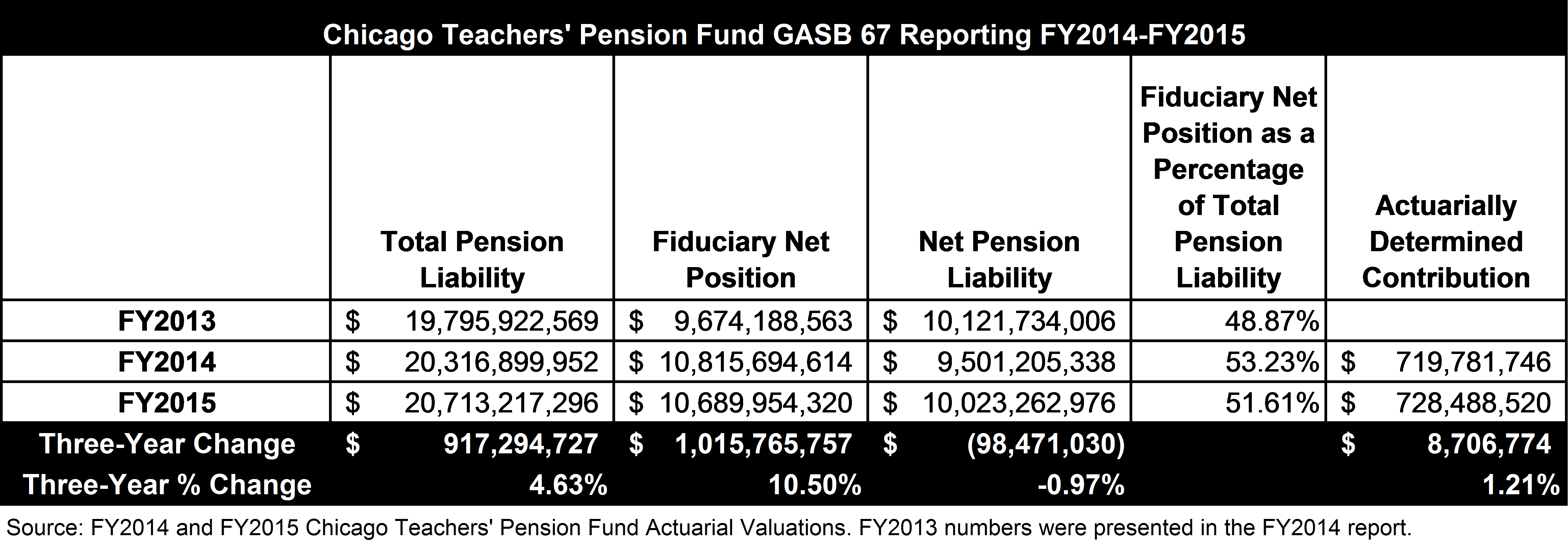

Chicago Teachers’ Pension Fund Reported Liabilities Under GASB Statements Number 67 and 68

The following table shows the Chicago Teachers’ Pension Fund (CTPF) pension financial reporting under GASB 67 and 68. Fiduciary Net Position as a percentage of Total Pension Liabilities is analogous to a funded ratio as calculated under actuarial standards. In contrast to other Chicago-area governments, CTPF’s pension liability reporting under GASB 67 and 68 is not significantly different from its statutorily reported numbers calculated on an actuarial basis. The reason is that projected assets are forecast to be sufficient to cover projected benefit payments and therefore the full expected rate of return on assets can be used as a discount rate. Other local governments have been projected to reach such a crossover point beyond which projected benefit payments will exceed assets and therefore must use a lower discount rate, which results in higher present values for liabilities and net pension liabilities.[3]

[1] Governmental Accounting Standards Board, Pension Standards for State and Local Governments. Available at: http://www.gasb.org/jsp/GASB/Page/GASBSectionPage&cid=1176163528472.

[2] Other differences and newly reported numbers are not central to the discussion here.

[3] For more on discount rates and how they impact measurements of the present value of liabilities, read the Civic Federation blog posts: https://www.civicfed.org/iifs/blog/state-pension-liabilities-rise-due-lower-expected-investment-returns and https://www.civicfed.org/civic-federation/blog/local-government-pension-funds-lower-their-expected-investment-rates-return-fy.