November 21, 2011

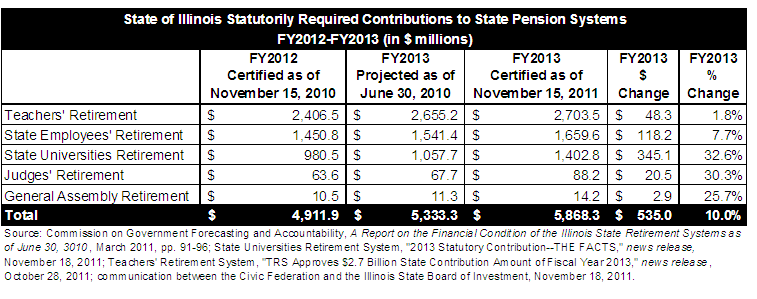

The State of Illinois’ statutorily required contributions to its five retirement systems will be $535.0 million higher than expected in FY2013, partly due to the impact of a pension reform law enacted in 2010.

Required FY2013 state contributions to the five systems had been projected to total approximately $5.333 billion, based on actuarial valuation reports as of June 30, 2010. The retirement systems are the Teachers’ Retirement System (TRS), the State Employees’ Retirement System (SERS), the State Universities Retirement System (SURS), the Judges’ Retirement System (JRS) and the General Assembly Retirement System (GARS).

As shown in the table below, updated actuarial reports as of June 30, 2011 increased the required contributions to $5.868 billion. Under the Illinois Pension Code (40 ILCS 5) each retirement system must certify to the Governor the state contribution needed for the next fiscal year by November 15 of the current fiscal year. Illinois’ fiscal year begins on July 1 and ends on June 30.

The Governor includes the certified state pension contributions in his annual budget recommendation, which is issued on the third Wednesday in February. The total FY2013 contribution is now expected to be $956.4 million higher than the total FY2012 contribution of $4.912 billion.

Illinois pensions are funded under a 50-year plan that took effect in July 1995 (Public Act 88-0593). After a phase-in period of 15 years, the law requires State contributions at a level percentage of payroll sufficient to achieve a 90% funded ratio by the end of FY2045. A funded ratio shows the percentage of accrued liabilities that are covered by assets held by the systems’ investment funds.

In April 2010, legislation (Public Act 96-0889) was enacted that created a two-tier benefits system with lower benefits for state and many local government employees hired on or after January 1, 2011. The new tier of benefits includes a cap on the maximum pensionable salary of $106,800 in 2011, with future increases in the cap equal to the lesser of ½ of the increase in the Consumer Price Index and 3%.

If State contributions are calculated as a level percentage of capped payroll for new employees, then those contributions must be higher in the earlier years. Higher contributions in the earlier years are needed to offset decreasing payroll growth in later years when the workforce is increasingly made up of employees hired on or after January 1, 2011.

TRS took this change into account in its actuarial valuation as of June 30, 2010, according to a system spokesman. The $2.704 billion FY2013 contribution for TRS that was certified as of November 15, 2011 is only 1.8% higher than the $2.655 billion that was projected as of June 30, 2010.

The other four State retirement systems, however, incorporated the change only in their latest actuarial valuations, according to draft copies of their valuation reports as of June 30, 2011. The draft report for SURS states that the 2010 pension reform legislation did not specifically address whether State contributions would be calculated as a level percentage of capped payroll for new hires. In the latest valuation report, the system’s actuary assumed State contributions would be based on capped payrolls.

The certified FY2013 State contribution for SURS increased by $345.1 million, or 32.6%, from the June 30, 2010 valuation. SURS stated in a fact sheet issued on November 18, 2011 that $105.3 million of the increase was due to the impact of capped salaries for new hires. The remainder of the $345.1 million was attributed to a decrease in assumed future payroll growth due to reduced inflation and wage growth and changes in other actuarial assumptions, such as increased life expectancies.