February 24, 2017

As Illinois endured its 20th month without a complete budget, Governor Bruce Rauner proposed a financial plan for the upcoming fiscal year with a significant operating deficit and no details on how to address the State’s multi-billion backlog of unpaid bills.

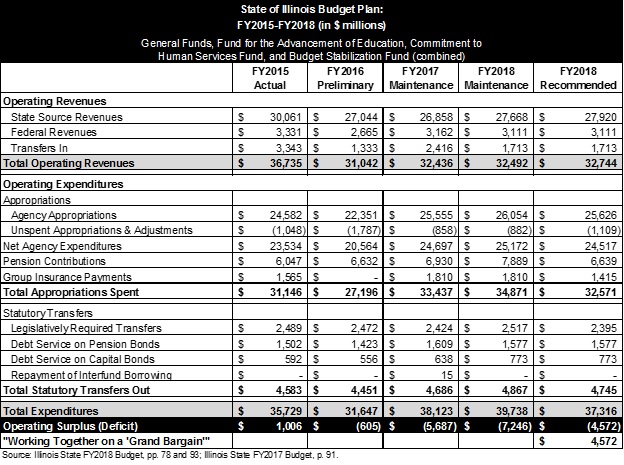

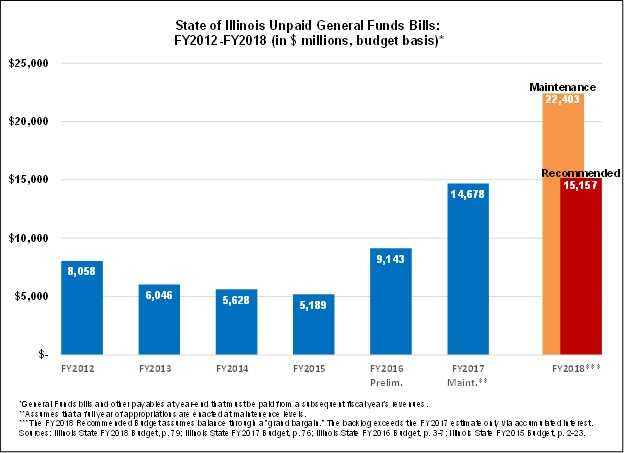

The recommended budget for fiscal year 2018 has general operating revenues of $32.7 billion and expenditures of $37.3 billion, resulting in a budget gap of $4.6 billion. The proposal also shows up to $15.2 billion of unpaid bills at the end of the fiscal year on June 30, 2018.

Instead of providing a specific plan to end the crisis, the FY2018 proposal relies on the success of a bipartisan effort by leaders of the Illinois Senate. The components of the legislative package, known as the grand bargain, are still fluid, but they generally include spending cuts, tax increases and policy changes, as well as the sale of bonds to pay down the bill backlog.

In his budget address on February 15, Governor Rauner said he could support the Senate plan under certain conditions: no State tax on retirement income; no permanent increase in income tax rates without a permanent freeze on property taxes; no increased sales tax rates for food and drugs (but he was open to taxing services); and a firm limit on spending. The Governor continued to press for term limits for lawmakers and reforms to the workers’ compensation system but said no single demand was essential.

However, it remains to be seen whether the legislation will be approved by the Senate or even considered by the Illinois House. If no bargain is enacted, Governor Rauner said he would seek broad authority to make cuts on his own to balance the budget.

This approach is similar to the Governor’s FY2017 budget recommendation, which had an operating deficit of $3.5 billion. That proposal offered legislators a choice of closing the gap with additional revenues, if they agreed to pro-business policy changes, or granting Governor Rauner the power to slash spending. The General Assembly declined to authorize either option.

As discussed in this report, Illinois has not had a comprehensive budget since FY2015 because of a political dispute between Democratic legislators who control the General Assembly and the Republican Governor who took office in January 2015. State government has continued to function largely because of court orders, consent decrees and statutory requirements.

A stopgap appropriations package—signed on June 30, 2016 and expiring on December 31, 2016—provided partial relief for most areas of government that had received little or no State funding since the end of FY2015: higher education, human services and agency operations. But it did not cover employee group health insurance, which has not obtained general operating funds since the deadlock began.

Governor Rauner’s FY2018 budget includes additional appropriations for these areas in FY2017, which ends on June 30, 2017. At a Senate hearing on February 16, administration officials said no supplemental spending will be approved for FY2017 without a comprehensive budget plan in place for FY2018.

The following table summarizes the proposed General Funds budget for FY2018. It also shows actual results for FY2015 and preliminary results for FY2016. For FY2017, the numbers include supplemental appropriations needed to maintain historical spending patterns. Similarly, FY2018 maintenance shows estimated expenditure levels with no changes in law or spending controls.

Recommended FY2018 spending of $37.3 billion is $2.4 billion below the FY2018 maintenance level of $39.7 billion. Proposed savings include:

- Pensions: Contributions to the State’s poorly funded retirement systems would decline to $6.6 billion, which is about $1.25 billion below the amount currently required by State law.

- About $500 million of the savings would come from requiring local school districts and universities to cover all pension costs for new employees, leading to a significant decrease in the State’s future pension obligations. This results in a sharp decline in current contribution requirements because of the State’s pension funding formula.

- The remaining savings would be based on the same pension changes recommended in the FY2017 budget: ending salary spiking, reallocating pension costs for high-salary employees, smoothing the impact of assumption changes and basing the funding formula on full payroll.

- Group Health Insurance: Payments would decline by $435 million, or about 24% from the FY2018 maintenance level, reflecting the reduced benefits offered by the administration in labor negotiations. The State’s largest employee union is fighting those terms in court and voted on February 23 to authorize its first strike against Illinois.

- Employee Compensation: The State would save about $336 million through a four-year freeze on employee wage increases, except for merit pay bonuses, under the contract terms being disputed in court.

- Procurement: Streamlining the State’s purchasing processes is expected to save $174 million.

- Senior Care: Spending is cut by $120 million by providing less costly home and community services for seniors who do not qualify for Medicaid.

- Other: In addition to the cuts highlighted in the budget, the administration proposes to eliminate human service programs including youth employment, after-school programs for teens, indigent funerals and immigrant support services.

The FY2018 budget also includes the following spending increases from the maintenance level:

- Education: Spending on elementary and secondary education would increase by $250 million, including an additional $145 million for transportation, $50 million for early childhood education and $30 million for General State Aid. Higher education funding declines by $125 million overall, but that includes a $36.5 million increase for Monetary Award Program grants to low income college students and $74.1 million for performance based funding.

- Childcare: The threshold for financial assistance for childcare for working families would be restored to 185% of the federal poverty level from 162%, where it had stood since November 2015.

- Public Safety: A projected 170 new State troopers would be trained at a cost of $10.5 million.

Projected FY2018 revenues of $32.7 billion include $300 million from the proposed sale of the James R. Thompson Center in Chicago. The net impact of the sale is estimated at $240 million, after accounting for expenses to relocate the 2,200 State employees who work in the building.

Even if the Governor and the General Assembly are successful at balancing the FY2018 budget through a grand bargain, the State still must address the deficits of past years, which through deferred payments have accumulated into a large bill backlog. The history and projections of the backlog are shown in the chart below.

The backlog estimates presented above are on a budgetary basis and are intended to show accounts payable and other liabilities at the end of a fiscal year that will have to be paid from a subsequent year’s revenues. This is somewhat different from the backlog reported by the Comptroller, which represents outstanding bills at a point in time. The budgetary basis numbers include fiscal year-end General Funds payables—bills owed to vendors and payments and transfers owed to State agencies and local governments—that will be paid during the lapse period, as well as estimated Section 25 liabilities, which can be paid from subsequent years’ appropriations.

The ultimate amount of the backlog depends on both the outcome of FY2017 and a plan to address the backlog itself, neither of which is addressed in the FY2018 budget book. As shown in the chart above, the Governor’s Office of Management and Budget estimates that if FY2017 expenditures occur at maintenance levels, the year will end with a $5.7 billion deficit, which would be added to the backlog.

Since the second half of FY2017 expenditures have yet to be appropriated, it is within the State’s power to make meaningful cuts. Moreover, some new revenue measures to address the FY2018 deficit, if implemented immediately, would provide additional revenues in FY2017 as well.

However, even in the unlikely scenario that FY2017 ends with no deficit, the backlog left over from FY2016 would continue to grow due to interest costs. A significant portion of the backlog earns interest at either 9% or just over 12% annually. The Governor’s recommended budget proposal as written assumes a balanced budget in FY2018, but shows that the backlog would increase by an estimated $479 million, from the end of FY2017 to the end of FY2018, based on interest costs alone.

Therefore, even if the State balances its budget through a grand bargain in FY2018, it still faces a choice. It could do nothing about the backlog left over at the end of FY2017 (at whatever level it ultimately reaches), in which case the total backlog amount will continue to rise due to interest.

Or it could take steps to address the backlog. Paying the bills directly would require additional revenues or expenditure cuts, the amount of which depends on how quickly the backlog is paid off. Borrowing is the fastest method of eliminating the backlog and could potentially save on interest costs, but would also require additional revenue or cuts to cover the debt service.

In the Senate’s proposal to pay off the backlog through a bond issuance of $7 billion, debt service payments are estimated at $1.1 billion for the next seven years. Adding direct backlog payments or debt service to the $4.6 billion needed to close the FY2018 deficit will make the choices needed to achieve a grand bargain significantly more painful.