March 08, 2013

On March 6, 2013, Governor Pat Quinn issued his recommended budget for the fiscal year that begins on July 1, 2013. However, the first major obstacle to the Governor’s proposed FY2014 budget emerged a day earlier, when the Illinois House approved a revenue projection that was significantly below the Governor’s revenue number.

The Governor’s budget recommendation is based on projected FY2014 General Funds revenues of $35.6 billion. The House estimated that General Funds revenues in FY2014 would be $549 million lower at $35.1 billion.

The General Funds revenue projection has recently played a key role in the legislature’s budget process. For the past three years, the General Assembly has begun its work on the budget by adopting a revenue projection that establishes a spending limit for the next fiscal year.

This was the first year that a legislative revenue estimate was approved prior to the release of the Governor’s budget. The House adopted House Resolution 83 on March 5, 2013 by a vote of 100 to 15. During the discussion of HR83 on the House floor, it was noted that the Governor’s revenue number was expected to be above the House projection and that approval of the measure would put the House at odds with the Governor’s spending plan.

The General Funds revenue projection approved by the House matched the revenue analysis published on February 3, 2013 by the staff of the legislature’s Commission on Government Forecasting and Accountability (COGFA). The Governor’s estimate was based on a projection by the Illinois Department of Revenue in consultation with the Governor’s Council of Economic Advisors.

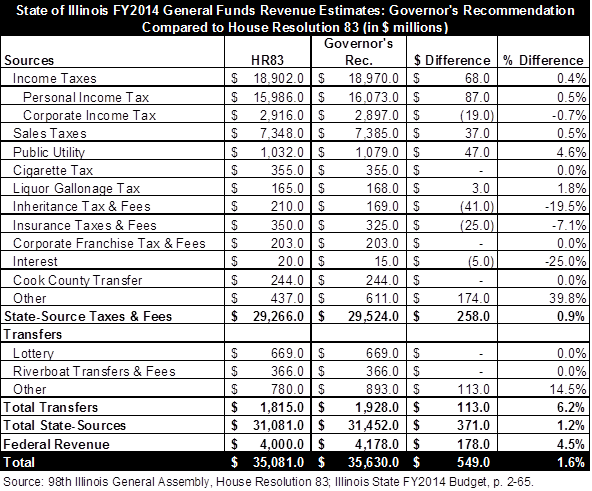

The following table compares the General Funds revenue projection included in the Governor’s recommended FY2014 budget and the amounts included in HR83 by revenue source. (Click to enlarge.)

According to the Governor’s budget officials, the difference in revenue projections is mainly related to income tax refunds. The Governor’s FY2014 estimate includes a transfer from the Income Tax Refund Fund of roughly $150 million due to an anticipated surplus in the fund in FY2013. The Illinois Income Tax Act requires that any surplus in the fund at the end of the year be transferred into General Funds in the following fiscal year. As discussed here, the Refund Fund holds income tax revenues diverted from general operating funds to pay income tax refunds owed to individuals and businesses. The State had previously built up a backlog of unpaid refunds owed to businesses and COGFA did not account for the new surplus, according to administration officials.

Due to the anticipated surplus, the Governor’s recommended budget also assumes that the percentage of income tax revenues diverted to pay refunds—known as the Refund Fund Rate—will decline in FY2014. A lower Refund Fund Rate means that a larger share of revenues will be available for general operating purposes. The Governor’s budget shows the Refund Fund Rate declining from 9.75% in FY2013 to 9% in FY2014 for personal income taxes and from 14% to 12% for business income taxes. COGFA’s revenue projection assumes that these rates are left unchanged in FY2014.

As shown in the table above, the Governor’s recommended FY2014 budget also anticipates more federal revenues in FY2014 than the projection adopted by the House. Federal revenues in the General Funds budget mainly reflect reimbursements for State Medicaid spending.

Since the General Assembly began setting spending caps based on revenue forecasts, the annual budget passed by the legislature has used the estimates originating in the House. The Governor made his budget recommendation for FY2012 on February 16, 2011 and the House adopted House Resolution 110 on March 8, 2011. The Senate adopted its own measure, Senate Joint Resolution 29 on March 17, 2011, but the budget passed by the General Assembly reflected HR110.

The FY2013 budget recommendation by the Governor was presented on February 22, 2012. The House adopted House Resolution 707 on March 1, 2012 and the Senate adopted the identical Senate Resolution 586 on March 7, 2012.

After approving the revenue projection as the coming year’s spending cap, the General Assembly continues to develop the budget by passing measures allocating available resources for each fiscal year. This involves first accounting for nondiscretionary costs such as pension payments, debt service, State group health insurance and statutorily required transfers before dividing the remaining resources among the appropriations committees to fund agency budgets. In FY2013 the spending resolution also set aside a specific amount to pay down a portion of the State’s backlog of unpaid bills.

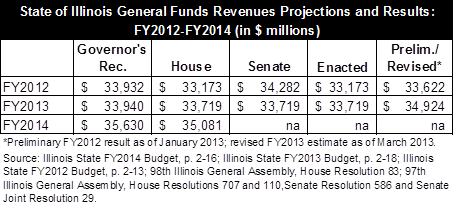

The following table shows the revenue projections in the Governor’s recommended budget, legislative projections, enacted budgets and revisions for FY2012 and FY2013 compared to the FY2014 projections. The largest sources of revenue to the State, income taxes and sales taxes, are economically sensitive and can vary from projections and enacted estimates. The changes occur for a variety of reasons including unanticipated shifts in employment rates and business cycle changes. Altered federal and State tax policies during the fiscal year can also influence actual revenue outcomes. (Click to enlarge.)