March 10, 2010

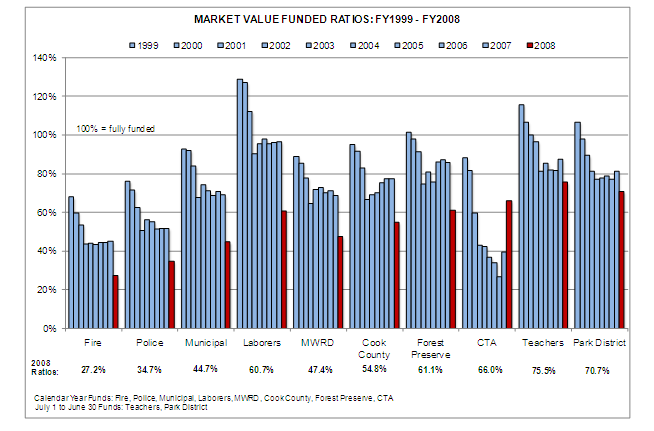

As reported in the Civic Federation’s latest report on ten local government pension funds, the most recent audited financial statements of the Chicago firefighters’ pension fund showed a market value funded ratio of only 27.2%. The Chicago police fund was close behind at only 34.7%.

What do these numbers mean?

Funded ratio is the most basic indicator of pension fund status. It is the ratio of assets to liabilities and can be expressed using either the current market value of assets or using a smoothed value of those assets that recognizes deviations from expected returns over a period of three to five years. Many funds report smoothed asset values as the official actuarial value of assets because current market values can be volatile and year-to-year variations typically average out over the life of the pension plan. In July 2009 the Illinois General Assembly passed legislation requiring the five State of Illinois pension funds to change from using current market value of assets to a five-year smoothed value of assets.

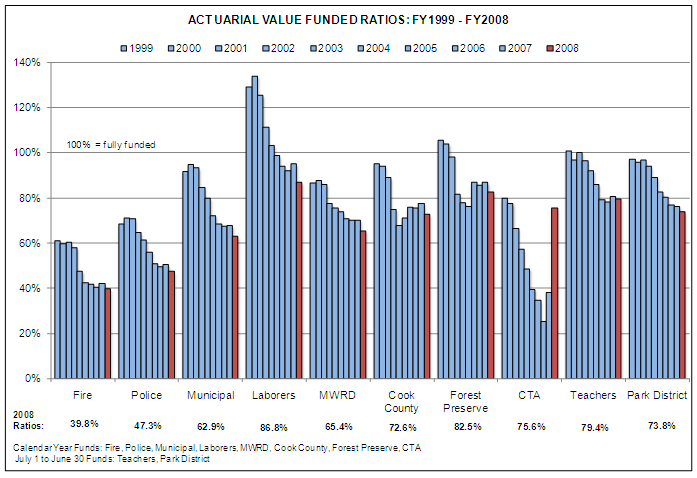

However, a funded ratio based on a smoothed actuarial value of assets does not represent the percentage of liabilities that could be covered by assets if those assets were sold at their current market value. For example, the Chicago Fire fund had a 2008 actuarial value funded ratio of 39.8% but a market value funded ratio of only 27.2%. In other words, the 2008 market value of assets was equal to only 27.2% of actuarial accrued liabilities. During a period of substantial investment gains or losses, a smoothed actuarial funded ratio does not reflect the true level of assets held by the fund.

When a pension fund has enough assets to cover all its accrued liabilities, it is considered 100% funded. This does not mean that employer and employee contributions are no longer required, but rather that the plan is funded at the appropriate level on the date of valuation. A funding level under 100% means that a fund does not have sufficient assets on the date of valuation to cover its actuarial accrued liability.

Some people claim that there is no real need for governments to achieve 100% funding, although federal law requires that private sector pension plans meet a 100% funding target.[1] They argue that governments, unlike private corporations, are not at risk of dissolving and, therefore, can meet their obligations in perpetuity. However, if the unfunded liability is growing and the plan has no practical strategy for reducing it, this is cause for serious concern.

Most market value funded ratios for the ten Chicago-area public pension funds declined since fiscal year 1999, and dropped dramatically in fiscal year 2008. The one exception is the CTA fund, which received $1.1 billion in pension obligation bond proceeds in 2008.

The smoothed actuarial funded ratios of all funds except the CTA (due to the infusion of $1.1 billion in bond proceeds) have also fallen since 1999, and every fund except the Laborers and Forest Preserve is less than 80% funded.

[1] See the Pension Protection Act of 2006, Public Law 109-280, http://frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=109_cong_public_laws&docid=f:publ280.109.pdf . See also Deloitte, “Securing Retirement: An Overview of the Pension Protection Act of 2006,” (August 3, 2006) http://www.hreonline.com/pdfs/01012007Extra_Pension_SecuringRetirement.pdf. The Worker, Retiree and Employer Recovery Act signed into law by President Bush on December 23, 2008 loosened some of these requirements by, for example, extending from 10 to 13 the number of years an “endangered” (less than 80% funded) plan is given to implement an improvement strategy. See the Worker, Retiree, and Employer Recovery Act of 2008, HR 7327, Public Law 110-458, http://frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=110_cong_bills&docid=f:h7327enr.txt.pdf