April 28, 2010

The third and final part of the Civic Federation’s Frequently Asked Questions about township government in Cook County presents basic information about township government finances using FY2007 audited financial statements. The FAQ does not include information about the Town of Cicero, which is difficult to compare to other Cook County townships because it operates as both a township and a municipality.

Please click here for Part 1 and Part 2 of the FAQ.

For the purposes of this FAQ, the Civic Federation aggregated and compared data for the 24 Cook County townships with comparable data. Townships with comparable data are those that reported their FY2007 Financial Statements in modified accrual accounting and did not have a memorandum only total for governmental funds. Five townships were excluded under this comparison criterion. Townships with comparable data include all townships except the Townships of Norwood Park, River Forest and Worth, which had memorandum only totals for governmental funds in FY2007; Barrington Township, which presented its FY2007 Financial Statements in the cash basis of accounting; and Elk Grove Township, which presented its Financial Statements in the cash with assets method of accounting.

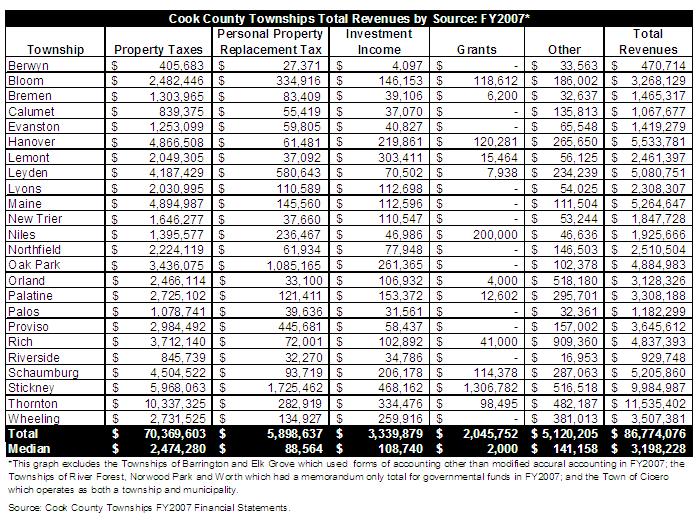

What are the Cook County townships’ major sources of revenue?

Townships primarily fund their governmental operations from tax revenue, particularly property taxes and personal property replacement taxes.[1] Townships also receive funding from investment income, grants and other sources. Townships with comparable data in FY2007 had total revenues of $86.8 million. The majority of revenue, approximately 81.1%, came from property taxes. The second largest revenue source was the personal property replacement tax, which made up 6.8% of total revenues. The third largest revenue source was revenues from other sources, which constituted 5.9% of total revenues. Investment income and grants made up the smallest share of revenue, making up 3.8% and 2.4% of total revenues, respectively. The following table summarizes FY2007 revenues by source for Cook County townships with comparable data.

How much do Cook County townships spend?

Township government total expenditures vary, but their total expenditures are generally lower than those of overlapping local governments. Townships with comparable data had total government fund expenditures of $78.9 million. For townships with comparable data, township expenditures for FY2007 ranged from as high as $10.1 million in Thornton Township to as low as $406,663 in Berwyn Township. The median total governmental funds expenditure in FY2007 was $2.6 million.

The following bar graph summarizes total FY2007 township expenditures in governmental funds for townships with comparable data.

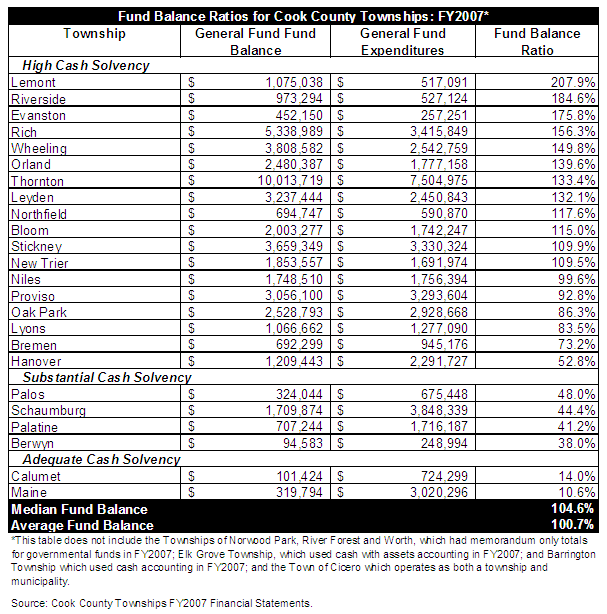

Cook County township fund balances, a measure of the financial resources available in a governmental fund, vary in size but tend to run high. The Civic Federation examined fund balances in the townships’ General Funds, because resources in these funds are not restricted for any specific purpose. The resources in other township special purpose funds, such as funds for General Assistance and Roads and Bridges, are restricted for those purposes.

The Government Finance Officers Association (GFOA) recommends that general purpose governments maintain at a minimum an unrestricted General Fund balance of no less than two months of regular General Fund operating revenues or regular General Fund operating expenditures. This amounts to 16.7% of either General Fund operating revenues or regular General Fund operating expenditures.[2] Township governments are not general purpose governments, but it is prudent for all governments to have adequate fund balances.

The Civic Federation calculated the fund balance ratio of the General Funds of each township with comparable data by dividing the FY2007 fund balance of the General Fund by total General Fund expenditures. Ratios resulting from the calculation are classified as follows:

- If the current fund balance ratio is less than 10%, the government can be said to have “Low” cash solvency;

- If the current fund balance ratio is at least 10% but less than 25% of spending, the government can be said to have “Adequate” cash solvency;

- If the current fund balance ratio is greater than 25% but less than 50%, the government can be said to have “Substantial” cash solvency; and

- If the current fund balance ratio is greater than 50%, the government can be said to have “High” cash solvency.

The following table summarizes township fund balance ratios at the end of FY2007 for Cook County’s townships. Townships are categorized by the criteria developed by the Civic Federation. Of the 24 townships with comparable data in FY2007, 18 townships had high cash solvency, 4 had substantial cash solvency and 2 had adequate cash solvency. Fund balance ratios of the General Funds amongst these townships range from as low as 10.6% in Maine Township to as high as 207.9% in Lemont Township. The 24 townships had a median fund balance ratio of 104.6%.

Twelve of the townships had a fund balance ratio higher than 100%, meaning these townships had a General Fund reserve equivalent to at least 12 months of General Fund expenditures. Notably, Lemont Township had a General Fund reserve equivalent to over two years of General Fund Expenditures. Six townships had General Fund reserves equivalent to between 6 months and 12 months of General Fund expenditures. Four townships had General Fund reserves equivalent to between 3 months and 6 months of General Fund expenditures. Two townships had General Fund reserves equivalent to between 1 to 2 months of General Fund expenditures.

The following graph summarizes FY2007 fund balance ratios for Cook County townships with comparable data.

.png)