July 17, 2015

On July 15, 2015, the Cook County Board of Commissioners voted 9-7 to once again increase the county sales tax by one percentage point, taking effect on January 1, 2016. Once in place for one full year, Board President Toni Preckwinkle’s office projects that the tax hike will generate nearly $474 million in revenues and proposed that revenues be dedicated to start to pay down the County’s $6.5 billion in pension obligations and to fund infrastructure projects. The County’s portion of the sales tax was previously increased by one percentage point in 2008 and was subsequently lowered over the following years, returning to the previous level as of January 1, 2013.

Those who supported the sales tax increase argued that it was necessary because pension obligations are costing Cook County $1.0 million per day and that without pension reform in Springfield the County would have to make more than the previous cuts that closed budget deficits of $1.4 billion. The commissioners who voted against the resolution argued that the sales tax increase will be detrimental to businesses and constituents in Cook County. The commissioners fear that businesses that border the collar counties as well as Indiana will suffer the most because consumers will take their business to areas with lower tax rates or will purchase items from the internet. Many also argued that the sales tax is a regressive tax that will harm those who already struggle financially.

The Civic Federation did not support the increase to the Cook County sales tax because it is not tied to a budget plan and County Commissioners should not be asked to vote on such a significant revenue increase in the abstract. Some Commissioners made the same argument. The Civic Federation acknowledges that the County requires increased revenues to adequately fund its pension obligations in the future, but cautions that relying on a single, economically sensitive revenue source like the sales tax might prove problematic. The sales tax has a history of disproportionately negative impacts on border areas and the one cent increase will burden Chicago taxpayers with the highest aggregate sales tax in the nation. The Civic Federation urges the County to continue to pursue pension reform in Springfield in order to lower the future burden on taxpayers.

As mentioned above, this is not the first time the Board of Commissioners has voted to increase the sales tax. Most recently, on July 1, 2008, a one percentage point sales tax increase went into effect in Cook County raising the home-rule tax from 0.75% to 1.75%. While then-Board President Todd Stroger said the tax increase was necessary to fund county services, the Civic Federation opposed the budget proposal partly because the County did not first demonstrate the will and ability to contain spending before proposing increased revenues. The increase brought the City of Chicago’s composite sales tax rate on general merchandise to 10.25%, one of the highest rates in the region and the highest rate among major U.S. cities. The City of Chicago will again top both lists once the higher rate takes effect.

What is the Sales Tax?

“Sales” taxes in Illinois are actually composed of two matching pairs of taxes: retailers’ occupation and use taxes and service occupation and use taxes. For simplicity, we refer to them as sales taxes. There is also a sales tax on general merchandise that applies to tangible items except food and drugs but including alcoholic beverages, soft drinks and food prepared for immediate consumption, for example in a restaurant. Various exemptions apply. The sales tax on food and drugs that applies to food purchased for consumption off the premises, prescription and non-prescription drugs it is not discussed in this blog post. The composite, or total, sales tax rate on general merchandise in a community in Illinois depends on the rates charged by various local governments, but across the state, a 6.25% rate is charged by Illinois. Of this, one percentage point is distributed to municipalities. For all counties in Illinois, except Cook County, the state distributes 0.25% of the 6.25% to counties. In Cook County the 0.25% tax is collected by the state and allocated to the Regional Transportation Authority (RTA).

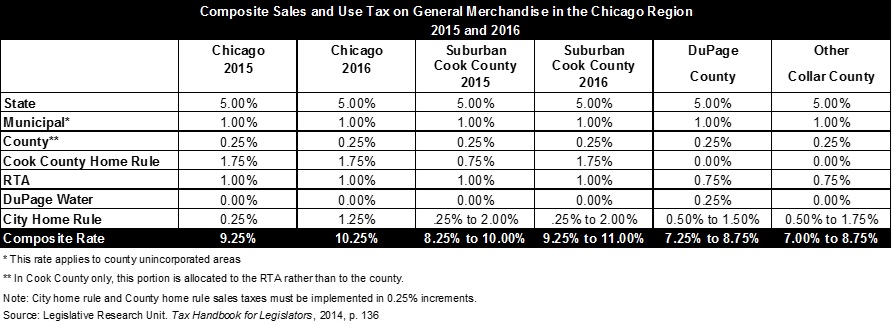

Composite Sales and Use Tax in the Chicago Region

The state of Illinois allows home rule municipalities, like the City of Chicago, and the home rule County of Cook to levy their own sales tax, subject to certain limitations. In the chart below these portions of the sales tax rate are called “home rule” to distinguish them from the portion of the sales tax automatically distributed to municipalities by the state of Illinois. The following table summarizes local government sales tax rates on general merchandise in Chicago, Suburban Cook County, DuPage County and other collar counties (e.g., Kane, Lake, McHenry and Will Counties) in 2015 and the new composite rates in effect in 2016 after the new tax rate goes into effect in Cook County.

On January 1, 2016, the composite sales tax in the City of Chicago will be 10.25% while the Cook County suburban sales tax rates will range from 9.25% to 11.0%. Even at the lowest rate of 9.25%, municipalities in suburban Cook County will pay 0.05% more on the dollar than the highest taxing municipalities in DuPage or any of the other collar counties. Residents in Chicago will pay 3 to 3.25 percentage points more than the residents of other collar counties or DuPage County who reside in the lowest taxing municipalities and 1.5 percentage points more than the highest taxing municipalities.

Comparison of Sales Tax Rates for Selected US Cities

If there are no legislative or statutory changes to the tax rates in the other cities listed in the table below, the City of Chicago is slated to have the highest sales tax rate of any other major municipality in the country beginning on January 1, 2016. Some of the cities in the table below were selected based on size, while others are selected because they are located in the Midwest. As of July 15, 2015, Chicago is currently tied with Memphis at 9.25% only behind Seattle at 9.5%, and Montgomery and Birmingham at 10.0%. However, beginning January 1, 2016, Chicago will have the highest sales and use tax rate of major municipalities in the United States. The closest cities to Chicago have substantially lower sales tax rates. Milwaukee and Madison both have rates of 5.6% which will be 4.65% lower than Chicago. Gary, which is just over the border, will be 3.25% less than Chicago.