May 22, 2013

This week the Civic Federation released its annual Status of Local Pension Funding report. The purpose of this report is to compile and analyze basic financial data of the retirement funds for the City of Chicago (four separate funds – Municipal, Laborers’, Police and Fire), Chicago Park District, Chicago Public Schools (Teachers’ Fund), Cook County, Forest Preserve District of Cook County, Metropolitan Water Reclamation District (MWRD) and Chicago Transit Authority (CTA). [1] The report explains common indicators of pension fund fiscal health and causes for change in the health of the local funds. It also reviews recent pension benefit changes. The report is intended to provide policymakers, pension trustees, pension fund members and taxpayers with information they need to make informed decisions regarding public employee retirement benefits. It reviews fiscal year 2011 actuarial valuation reports and financial statements of ten pension funds. Fiscal year 2011 data is the most recent audited data available for all ten pension funds.

Highlights of the data compiled on the ten pension funds are summarized below.

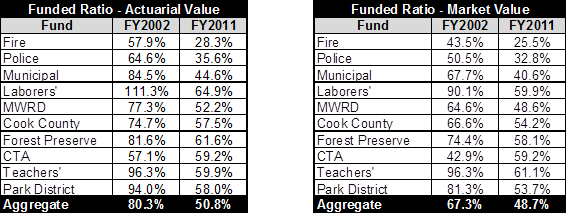

Funded Ratios: The actuarial value funded ratio of each fund fell in FY2011. All ten funds now have actuarial value funded ratios under 65%, ranging from a low of 28.3% for the Fire Fund to a high of 64.9% for the Laborers’ Fund. The actuarial value funded ratio for the aggregate of all ten funds’ assets and liabilities was 50.8% in FY2011, down from 80.3% in FY2002. Market value funded ratios were considerably lower, at an aggregate ratio of 48.7% in FY2011. The lowest market value funded ratio was the Fire Fund at 25.5%, and the highest was the Teachers’ Fund at 61.1%.

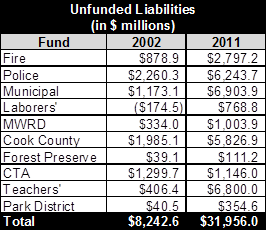

Unfunded Liabilities: Between FY2002 and FY2011 the aggregate unfunded actuarial accrued liabilities for the ten funds increased by $23.7 billion, rising from $8.2 billion to nearly $32.0 billion. Unfunded liabilities for the ten funds increased by $4.6 billion, or 16.7%, from FY2010. Unfunded liabilities per capita in Chicago for the ten local funds rose from $1,189 in FY2000 to $10,472 in FY2011. For the four City of Chicago pension funds alone, FY2011 unfunded liabilities were $16.7 billion, or $6,174 per capita.

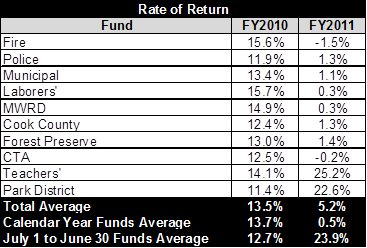

Investment Income and Rate of Return: The fiscal year for the Public School Teachers’ and Park District pension funds is July 1 – June 30. The other eight funds use a January 1 – December 31 fiscal year. The average rate of return on pension plan assets for those funds with a January 1 to December 31 fiscal year was 0.5% in FY2011, down from 13.7% in FY2010. The average rate of return for funds using a July 1 to June 30 fiscal year was 23.9% in FY2011, up from 12.7% in FY2010. Investment income represented an average of 24.5% of FY2011 pension fund income. [2]

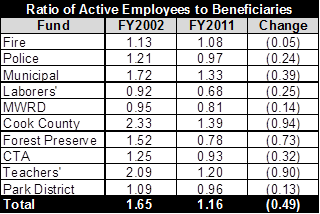

Ratio of Active Employees to Beneficiaries: Between FY2002 and FY2011, the ratio of total active employees to beneficiaries for the ten funds combined has gradually dropped from 1.65 actives per beneficiary to 1.16, indicating that there are fewer active employees supporting more retirees. The Police, Laborers’, MWRD, Forest Preserve, CTA and Park District Funds all had more beneficiaries than actives in FY2011.

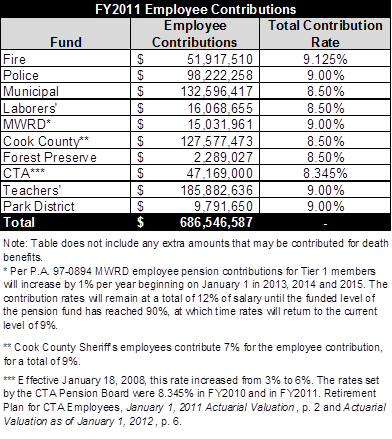

Employee Contributions: For all ten funds, employee contributions totaled $686.5 million in FY2011. Employees contribute at rates ranging from 8.345% to 9.125% of salary. [3]

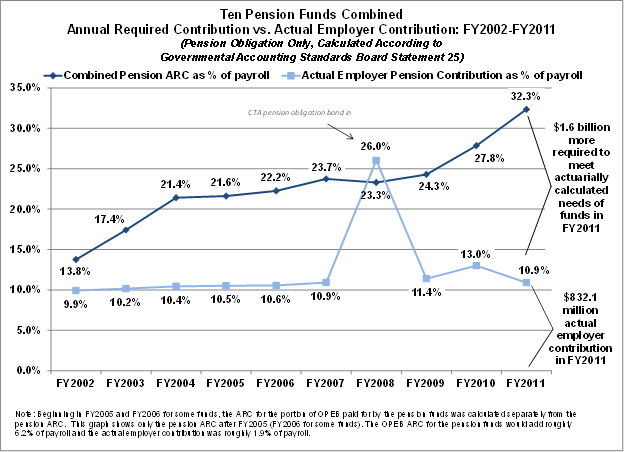

Employer Contributions and ARC: All funds received their statutorily required employer contributions in FY2011. However, none of the employers contributed the full actuarially calculated annual required employer contribution (ARC) in FY2011 and only one fund, the MWRD Retirement Fund, contributed more than 50% of the pension ARC. ARC is the sum of (1) the employer’s normal cost of retirement benefits earned by employees in the current year and (2) the amount needed to amortize any existing unfunded accrued liability over a period of not more than 30 years. ARC is a concept created and defined by the Governmental Accounting Standards Board. [4] In the aggregate, in order to meet the pension ARC in FY2011, employers should have contributed approximately $2.5 billion. Instead they contributed less than half that amount, $832.1 million, falling short by $1.6 billion. Employers contributed an aggregate equivalent of 10.9% of payroll to the pension funds for pension obligations. In order to meet the ARC, they should have contributed an additional 21.4% for a total of 32.3% of payroll in FY2011.

Civic Federation Recommendation for Pension Reform:

The deteriorating health of the ten pension funds featured in this report necessitates immediate action from local governments and the State to reform the current pension system. The Civic Federation recommends that local governments work together with the Illinois General Assembly to enact pension changes to significantly reduce pension costs, including reducing automatic annual benefit increases and raising the retirement age for current employees. Local governments must also pursue increased contributions from workers and changes to how governments fund their share of benefits, linking them to an actuarially sound methodology based on funding levels.

Local governments should develop their own frameworks for reform based on their funds’ individual characteristics, such as funding levels, population and statutory provisions. In 2012 the Metropolitan Water Reclamation District successfully developed and promoted a framework for pension reform which led to the enactment of Public Act 97-0894. The District’s reforms increase employee and employer contributions to the District’s pension fund in an effort to increase the Fund’s funded ratio. Recent efforts by Cook County Board President Toni Preckwinkle and Board Commissioner Bridget Gainer also provide an example of transparently advocating for reform. Commissioner Gainer’s OpenPensions.org website features reams of pension data and alternative scenarios and strategies for addressing the County’s pension problems with a focus on the ultimate goal of making its pension fund sustainable.

For more detailed information on the status of local pensions, read the full report here.

[1] The City of Chicago enrolls its employees in four different pension systems. The funds of Cook County and the Cook County Forest Preserve District are governed by the same pension board. Certified Teachers employed by the Chicago Board of Education participate in the Public School Teachers’ Pension and Retirement Fund of Chicago. Most other employees of the Board of Education are enrolled in the City of Chicago’s Municipal Employees’ Annuity and Benefit Fund. Approximately 16,061, or 52.3%, of Municipal Fund members considered to be active by the Fund are Board of Education employees. Chicago Public Schools, Comprehensive Annual Financial Report for the fiscal year ended June 30, 2011, p. 75. A very small number of Board of Education employees are enrolled in the Laborers’ Fund.

[2] The Civic Federation calculates investment rate of return using the following formula for all funds: Current Year Rate of Return = Current Year Gross Investment Income/ (0.5*(Previous Year Market Value of Assets + Current Year Market Value of Assets – Current Year Gross Investment Income)). This is not necessarily the formula used by all funds’ actuaries and investment managers, thus investment rates of return reported here may differ from those reported in a fund’s actuarial statements. However, it is a standard actuarial formula. Gross investment income includes income from securities lending activities, net of borrower rebates. It does not subtract out related investment and securities lending fees, which are treated as expenses.

[3] Of the ten funds covered in this analysis, only the participants in the CTA pension fund also participate in the federal Social Security program. CTA retirees are eligible for Social Security benefits in addition to their CTA pension benefits. The CTA and its employees each pay an additional 6.2% of the employee’s Social Security taxable salary to the Social Security administration. The majority of all government employers and employees hired after March 31, 1986 each pay Medicare payroll taxes of 1.45%. See Internal Revenue Service Publication 963 for further information.

[4] ARC is an accounting reporting requirement but not a funding requirement. However, it does represent a reasonable calculation of the amount of money the employer might contribute each year in order to cover costs attributable to the current year and to reduce unfunded liabilities.