October 20, 2011

Faced with mounting pension costs, the State of Illinois and a number of other states are considering moving away from traditional pension plans.

In traditional pension plans, formally called defined benefit (DB) plans, employers are responsible for a specified level of benefits at retirement, typically based on an employee’s earnings, length of service or both. In 401(k)-type plans, formally called defined contribution (DC) plans, employers are responsible for specified contributions but do not commit to provide specified benefits at retirement. Hybrid pension plans combine elements of DB and DC plans.

Employee participants in DB plans enjoy the assurance that they will have a secure and predictable level of retirement income. This assurance is particularly valuable for employees who are not covered by Social Security and thus do not have that additional safety net. However, guaranteeing pensions entails substantial risk for employers, who must ensure adequate pension funding. Employers bear the risks of poor investment performance, benefit enhancements, poor actuarial projections, governmental revenue declines and competing pressures on government resources. If assets are insufficient to cover pension obligations, employers must ultimately allocate resources intended for other uses to cover those commitments.

Most state and local government employees—87%—participated in DB plans in 2010, compared with 30% of private-sector workers, according to the Employee Benefit Research Institute. In contrast, only 19% of state and local government employees participated in DC plans, compared with 54% of private-sector workers.

Now more states are considering whether employees should share the risk for funding their retirements. States’ unfunded pension liabilities totaled $660 billion at the end of FY2009, according to the Pew Center on the States. While annual state pension payment requirements grew 152 percent from FY2000 to 2009, total state general operating spending rose only 44 percent.

Illinois’ five retirement systems had unfunded liabilities of $85.6 billion as of June 30, 2010 and a combined funded ratio of 38.3%, according to the General Assembly’s Commission on Government Forecasting and Accountability (COGFA). Although investment revenues declined sharply due to the market downturn in FY2008 and FY2009, the main cause of the growth in unfunded liabilities from FY1996 to FY2010 was insufficient state contributions, COGFA reported.

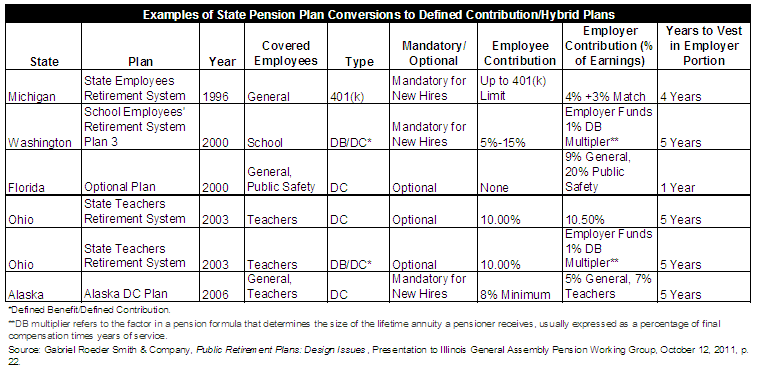

The table below shows examples of states that have created new DC or hybrid plans since the mid-1990s. It was part of an October 11, 2011 presentation by the actuarial firm of Gabriel Roeder Smith to a working group on pension reform organized by the Illinois General Assembly. In the table, DB Multiplier refers to the factor in a pension formula that determines the size of the lifetime annual payment a pensioner receives, usually expressed as a percentage of final compensation times years of service.

According to the presentation at the October 12 meeting, eight states including Illinois are considering implementing DC plans. The other states are Alabama, Connecticut, North Carolina, Nevada, Oklahoma, Tennessee and Wisconsin.

As of July 1, 2011, Utah has required new public employees to chose between a DC plan and a hybrid plan with DB and DC components. For the DB component, employers pay an amount up to 10% of an employee’s compensation toward the amount required to keep the plan actuarially sound (12% for public safety workers) and the employee contributes any additional amount needed to meet the actuarial requirement. For the DC component, employers contribute an amount equal to 10% of employee compensation less the amount the employer contributes to the DB component. The employer’s DC contributions are deposited in a 401(k) plan; employees may make additional contributions but are not required to do so.

A proposal announced on October 18, 2011 would create a hybrid pension plan in Rhode Island. Beginning on July 1, 2012, most employees would contribute 3.75 percent of their salaries to a traditional pension and 5 percent to a 401(k) retirement account. Automatic cost-of-living pension increases for retirees would be halted until the Rhode Island retirement system becomes more stable.

Proposed legislation in Illinois (Senate Bill 512) would offer state employees three choices, including a new DC plan. Those who were hired before January 1, 2011 could stay in the existing DB plan but would be required to make significantly higher contributions. In addition, employees could choose a reduced-benefit DB plan that was created for employees hired on or after January 1, 2011. Employee contributions to the new plan would be decreased from the current level.

In its presentation to the pension reform working group, Gabriel Roeder Smith representatives noted that when states move to DC plans, benefits accrued to members in the DB plan must still be funded and paid. When workers move to DC plans, they will not be helping to pay for the deficit in the DB plan, potentially requiring increased state contributions.

The Government Finance Officers Association (GFOA) has established best practices for designing DC and hybrid pension plans. For example, the GFOA recommends that DC plan designers determine the adequacy of the plan in meeting the needs of employees, design a sound investment structure and policy and design a participant education program. Employers considering a hybrid plan should assess the possible increased cost of administering additional plans or more complex plan features.