October 13, 2010

Cook County second installment property tax bills are expected to come out late this year and might not be due until December 22.

Will your bill be higher or lower than last year? It is very difficult to predict whether the tax bill for an individual parcel will increase or decrease in the future due to the complex interactions of many moving parts in the Cook County property tax system. The Civic Federation published a report last week describing how property tax rates are calculated, how tax increment financing (TIF) affects tax bills, and limitations on how much property tax revenue local governments can receive.

There are two major factors that affect year-to-year changes in a property owner’s tax bill:

- change in the property’s equalized assessed value (EAV) as a percentage of the total EAV of each taxing district with jurisdiction over it; and

- change in the taxing districts’ tax extensions as a percentage of the EAV under their jurisdiction.

Changes in EAV are a product of changes in assessed value (AV), the multiplier, and homeowner exemptions. The Civic Federation’s primer on the assessment process describes these three elements and their interaction. Change in an individual parcel’s EAV in relationship to the total EAV of a tax code is driven primarily by changes to AV and to a lesser extent by changes to homeowner exemptions, which reduce EAV.

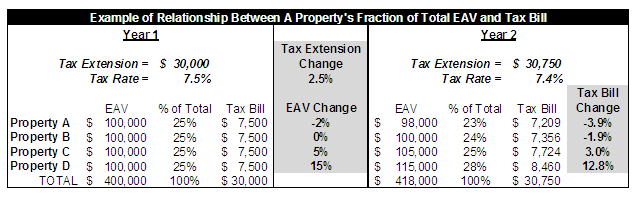

The table below provides a simplified demonstration of the relationship between these two factors. The example shows four properties in the same tax code with no TIF districts and uses a single taxing district with an extension of $30,000 in year one for the sake of simplicity. The four properties are of equal value in year one, thus each has 25% of total EAV and pays 25% of the tax extension. In year two, the taxing district increases its extension by 2.5%. However, the EAV of each property changes by a different amount: Property A falls by 2%, Property B remains the same, Property C increases by 5% and Property D increases by 15%.[1] These EAV changes increase the total EAV of the tax code by 4.5%, from $400,000 to $418,000 and shift the proportion of each property as a fraction of the total EAV. Because the tax extension increases by 2.5%, but the total EAV increases by 4.5%, the tax rate declines from 7.5% in year one to 7.4% in year two. The tax rate declined because total EAV grew more than the tax extension. This change in the rate caused changes in tax bills that were lower than the change in each property’s EAV:

- Property A’s EAV fell by 2% but its tax bill declined even more, by 3.9%.

- Property B’s EAV remained the same but its tax bill declined by 1.9%.

- Property C’s EAV grew by 5% but its tax bill increased by only 3.0%.

- Property D’s EAV grew by 15% but its tax bill increased by only 12.8%.

The results of this demonstration can easily shift by changing any one of the elements even slightly. For example, if Property A’s EAV had remained the same rather than declined by 2%, the tax bills would have declined by 2.4% for both Properties A and B, increased by 2.5% for Property C, and increased by 12.3% for Property D.

In reality, changes to individual parcels’ EAV have miniscule effects on the tax burden of other parcels due to the volume of EAV and the rounding of tax rates. In the aggregate, however, reductions in AV or increases in homeowner exemptions for many properties do have a real effect on the tax burdens of others.

The interrelationships between property EAVs and tax extension changes make it extremely difficult to reliably predict changes to individual tax bills. However, the demonstration illustrates how property taxes in Cook County are a zero-sum game, meaning that tax relief provided to one property owner must be paid for by all other owners because it affects both the total EAV upon which the rate is based and the proportion of total EAV for each property.[2] This zero-sum effect arises because the vast majority of non-home rule districts in Cook County are effectively limited by tax caps, not by fund rate limits (see the extension primer for more on these limits), so changes in EAV affect the tax rate and not the extension. The taxing district above still receives $30,750 in year two whether the total EAV is $400,000 or $418,000.