December 21, 2010

State and local governments utilize fund accounting in order to demonstrate accountability and compliance with rules, laws and regulations.[1] For example, Cook County has a multitude of funds including a Public Safety Fund, Health Fund, an Annuity and Benefit Fund, a Bond and Interest Fund and a variety of special funds. These funds help demonstrate how much the County is spending on an activity and how it is utlizing restricted revenues. The paradox of fund accounting is while it is intended to improve accountability it also adds complexity, which can make it more difficult to understand how tax dollars are being used.

As part of the Cook County Moderization Project the Civic Federation examined how the County allocates its tax revenues among funds. We found that the Public Safety Fund receives the largest share of all the tax sources other than the property tax.

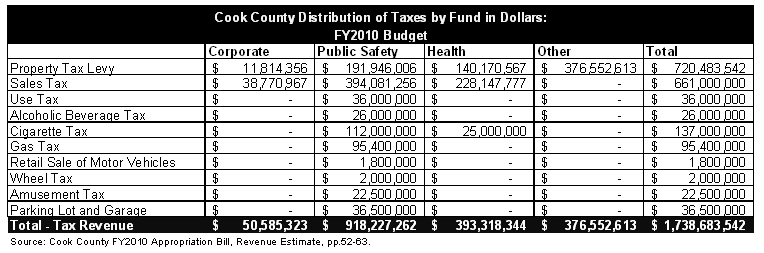

As illustrated in the following chart, the largest tax sources for the County are the property tax ($720.5 million), sales tax ($661.0 million) and the cigarette tax ($137.0 million).

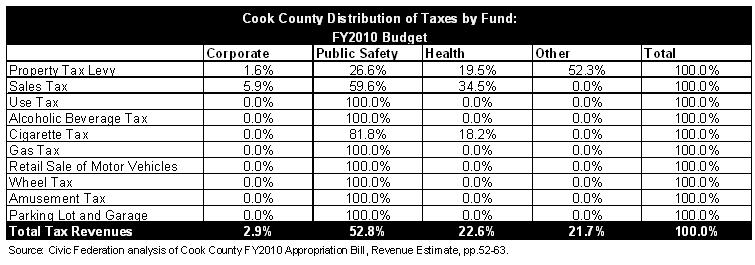

The next chart shows how the various taxes have been distributed to each County fund in FY2010 as a percent of the total. The Public Safety Fund and the Health Fund receive the vast majority of the sales tax revenue at 59.6% and 34.5% respectively. The remaining 5.9% is allocated to the Corporate Fund.

The Public Safety Fund and Health Fund also receive a significant amount of property tax revenue. The Public Safety Fund receives 26.6% and the Health Fund receives 19.5%. The Corporate Fund receives 1.6% of the property tax revenue. Over half of the property tax revenue is included in the other funds category in the chart, which includes the Election Fund, the Bond and Interest Fund and the Employee Annuity and Benefit fund.[2]

The majority of the cigarette tax is allocated to the Public Safety Fund (81.8%) with the remainder going to the Health Fund (18.2%). The Public Safety Fund also receives the entirety of the tax revenues from all taxes other than the property, sales and cigarette taxes. Receipts generated from the use tax, alcoholic beverage tax, gas tax, retail sale of motor vehicles, wheel tax, amusement tax and the parking garage lot and garage operations tax are all deposited directly or distributed in full to the Public Safety Fund. Overall, the Public Safety Fund receives 52.8% of tax revenues, the Health Fund receives 22.6%, other funds receive 21.7% and the Corporate Fund receives 2.9%.

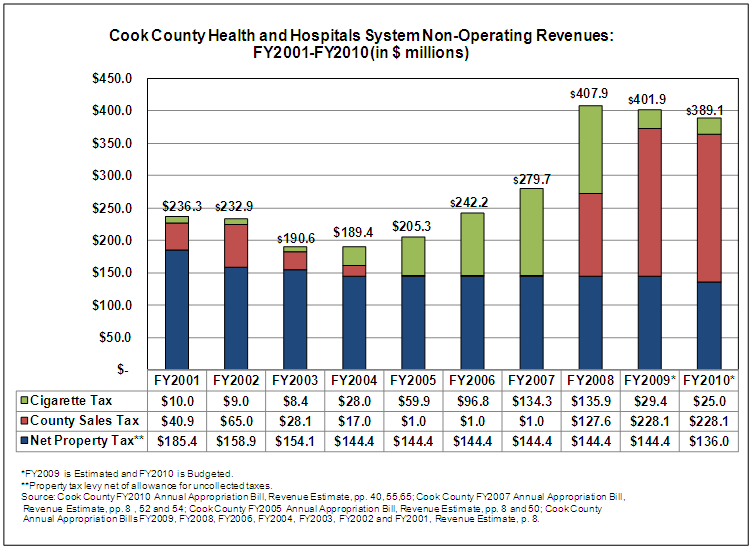

While it is interesting to examine the distribution of individual revenue sources it is also important to keep in mind the fungible nature of tax revenue. The distribution of County taxes received by the Health System demonstrates this interchangeable nature of the tax revenue. Property tax revenues going to the Health System have been stable while there has been substantial fluctuation in the amount of cigarette and sales taxes it receives. Following the increase in the County home rule sales tax rate from 0.75% to 1.75% in July 2008, the Health System has received a substantial share of sales tax revenues. Cigarette tax revenues allocated to the Health System were reduced following the increase in sales tax revenue. From FY2008 to FY2009 the individual taxes going to Health System changed significantly, but overall tax revenue going to the System did not as these changes offset one another.