June 27, 2011

The Illinois Department of Revenue has announced that the tentative equalization factor for the Cook County 2010 property assessment year (taxes payable in 2011) is 3.1773. The final equalization factor cannot be calculated until the Cook County Board of Review has finished hearing appeals and has certified the final assessments for 2010. That process may take several more weeks or months to complete.

What is the equalization factor and why do we need it?

Inter-county equalization (sometimes referred to as “state equalization”) is the application of a factor, or multiplier, to all assessed values such that the aggregate total equalized assessed value of all real property the county equals 33 1/3% of fair market value.[1] All counties, including Cook, are required to undergo equalization to ensure that the total value is 33 1/3%. Counties other than Cook also perform intra-county equalization in order to ensure that townships assessed by different assessing officials are equalized (35 ILCS 200/9-210).

Equalization is necessary for the fair implementation of certain state statutes. Assessed valuation of property is a component in formulas for various education, transportation and public assistance grants to local jurisdictions so it is important that assessed values be made equivalent statewide. State statutes that limit property tax rates and bonded indebtedness of local governments are also related to assessed value, which must be equalized in order for the statutes to apply equivalently across the state.

The State of Illinois Department of Revenue is responsible for calculating an equalization factor for each county. This calculation is made annually using a multi-year comparison of property assessments and sales prices in each county called the assessment/sales ratio study. This study is described in the IDoR’s Publication 136 and in the Civic Federation’s primer on the Cook County assessment process. The assessment/sales ratio study is used to compute a three-year adjusted average for the countywide median ratio, weighted by class of property. This 3-year average was 9.89% for Cook County in 2009, so the 2009 equalization factor was 3.3701 (33.33% ÷ 9.89%).

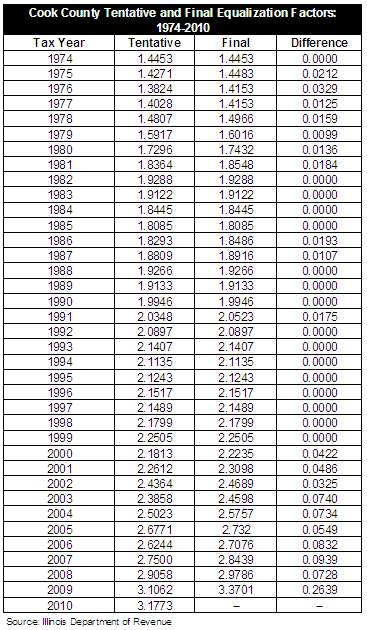

Before publishing a final equalization factor each year, the Department of Revenue calculates a tentative equalization factor and holds a public hearing on the tentative factor, per 35 ILCS 200/17-20. This tentative factor is computed before the Board of Review releases its final assessments for a given assessment year. For assessment year 2009, the Department released a tentative equalization factor of 3.1062 on June 10, 2010. The final factor of 3.3701 was published on September 29, 2010. The difference between the tentative and final factors is due to assessment reductions made by the Board of Review. The following table shows the difference between the tentative and final equalization factors from 1974 to 2009 and the tentative factor announced for 2010.

Once the Department of Revenue has certified the final Cook County equalization factor, the Cook County Clerk applies the factor to the final assessed values determined by the Assessor and modified by the Board of Review. The new value is called the equalized assessed value (EAV). This value is the final taxable value of the property unless homeowner exemptions are applied. For example, a Cook County home with a tax year 2009 assessed value of $32,000 would have an equalized assessed value of $107,843 ($32,000 x 3.3701equalization factor) before any homeowner exemptions were applied.

The increase in the equalization factor since 1974 reflects a decline in Cook County assessment levels as measured by the assessment/sales ratio. As the weighted average assessment level for Cook County properties falls farther below 33 1/3%, the equalization factor must increase to compensate. The equalization factor does not cause tax increases in Cook County, it simply compensates for the County’s low assessment levels.