March 31, 2026

By Lily Padula

This report is part of a three-part series on Illinois' proposed FY2027 budget. Click here to view the one-page summary of these reports.

Introduction

Governor Pritzker’s FY2027 budget proposal for the State of Illinois (Illinois or ‘the State’) largely reflects a “maintenance budget.” Overall, spending remains relatively flat or slightly higher compared with FY2026, with limited new initiatives and few major structural policy changes.

The proposal closes the $2.2 billion budget gap projected by the Governor’s Office in October 2025 primarily through a combination of targeted revenue changes, modest reallocations of existing revenues, and limited expenditure growth, rather than through large tax increases or deep spending reductions. Several of the budget-balancing measures involve temporary or incremental fiscal adjustments rather than permanent structural changes. These include extending limits on tax deductions, shifting revenues between funds, and adjusting the allocation of existing tax revenues.

This brief breaks down the major ways the Governor balanced his FY2027 proposal.

Overall Budget Balancing Strategy

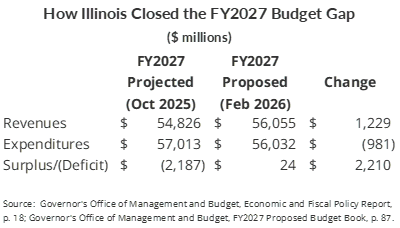

The proposed $56 billion FY2027 General Funds operating budget closes the previously expected $2.2 billion gap (3.9% of General Funds) with increased revenues of about $1.2 billion and decreased expenditures of nearly $1.0 billion. On the revenue side, increases are due to new revenue proposals, improved revenue projections, redirected existing revenues, and other incremental fiscal adjustments. On the spending side, the key driver is a $892 million decrease in General Funds support for medical assistance programs, partially offset by increased use of revenues from special purpose funds, supported in part by stronger revenue performance in certain funds (e.g., tobacco tax revenues). More generally, the proposal largely maintains existing programs and meets statutory spending requirements, rather than introducing major new initiatives. As the table below shows, October’s $2.2 billion budget gap is closed via combined revenue and expenditures adjustments, generating a modest $24 million surplus in FY2027.

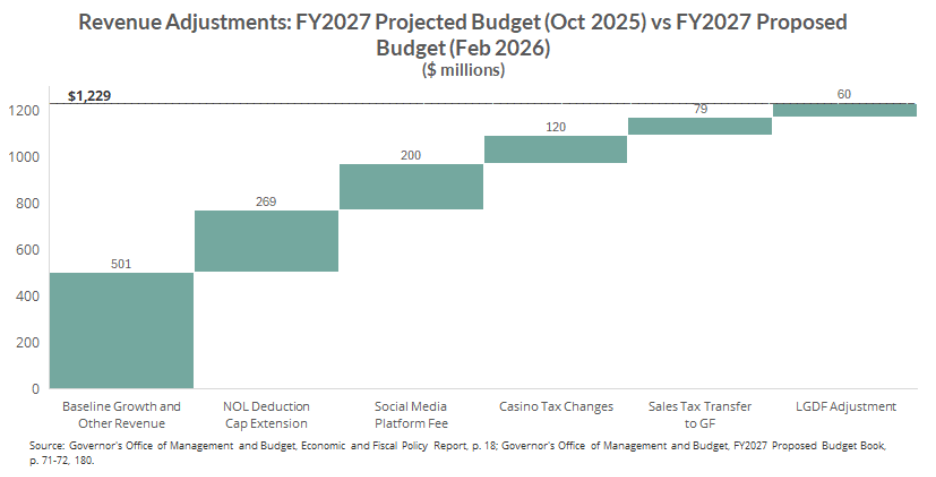

Revenue Adjustments

The Governor’s proposal increases revenue projections by $1.2 billion from the October forecast. Several actions shift the timing of revenues, while others reallocate existing revenue streams between General Funds and other funds. The budget proposal also includes new targeted revenue measures. The chart below depicts the key revenue adjustments, with a more detailed discussion to follow.

Baseline Growth and Other Revenue

A large portion of the projected FY2027 budget gap—$501 million—is closed through baseline revenue growth and other measures, reflecting updated revenue forecasts. The baseline revenue increase reflects the State’s updated economic forecast and stronger-than-expected collections in FY2026, particularly from the individual income tax and sales tax, which raised the starting baseline for FY2027. Because these increases occur under existing law and reflect updated economic and revenue forecasts, they are considered baseline revenue growth and are separate from the additional revenues generated by other new policy measures included in the proposed budget.

Other adjustments within this category reflect a combination of revenue reallocations and technical adjustments not specifically spelled out in the budget proposal. Together, these updates reduce the size of the projected shortfall identified in the fall fiscal outlook by approximately $500 million.

Timing: Extension of the Net Operating Loss (NOL) Deduction Cap

Since 2020, Illinois has placed limits on the amount of Net Operating Loss (NOL) deductions corporations can claim each year. These limits restrict the value of losses that corporations may deduct from taxable income, requiring firms to claim remaining deductions in future years. Under current law, corporations may deduct up to $500,000 per year in NOL carryforwards. This limitation effectively increases the amount of income subject to the State’s corporate income tax, resulting in higher near-term tax collections at the expense of future year collections.

The Governor’s FY2027 proposal would extend the existing cap for three years, after which the cap would phase out gradually, allowing corporations to claim larger deductions over several years until the full deduction is restored, delaying when corporations can claim the full value of accumulated losses. This extension is projected to increase General Funds revenue by approximately $269 million in FY2027.

New Revenues 1: Social Media Platform Fee

The proposed budget includes a new social media platform fee expected to generate approximately $200 million in FY2027. While details are still emerging, the proposal would impose a fee on large social media platforms operating in Illinois based on the number of platform users within the State.

Because similar policies have faced legal challenges in other jurisdictions, the proposal's ultimate fiscal impact may depend on how it is implemented and whether it withstands potential litigation.

New Revenues 2: Casino and Gaming Tax Changes

The budget proposal includes revisions to the casino tax structure, which are projected to increase state revenues by around $120 million. These changes involve adjustments to how revenue from table games is taxed, shifting to a graduated tax structure, and thereby capturing more revenue from higher-performing casinos. This change applies to 15 of the 16 casinos statewide, while excluding the Chicago casino, which has its own graduated tax structure.

Because gaming revenue tends to fluctuate with economic conditions and consumer behavior, the long-term stability of this revenue source may vary.

Shifting Revenues 1: Shifting Sales Tax Revenue to the General Funds

The proposal would shift approximately $79 million in sales tax revenue currently deposited in Capital Funds into the General Funds. Reallocating revenues between funds is a common budget-balancing strategy that provides short-term relief but does not represent a long-term best practice. While the policy increases available resources for operating expenditures, it also reduces funding available for capital purposes.

Shifting Revenues 2: Local Government Distributive Fund (LGDF) Adjustment

The Governor proposes a slight reduction to the LGDF percentage of state income tax revenues to local governments. Currently, local governments receive 6.47% of individual income tax receipts. The proposal would reduce this share to 6.23%. However, because overall statewide income tax revenues are projected to grow, local governments would still receive approximately the same funding as they currently receive. But that amount would be less than the expected growth in income tax revenues under the current formula. As proposed, local governments are held harmless (receiving the same revenue as last year), while State General Funds revenue would increase by approximately $60 million in FY2027. This additional revenue would have otherwise gone to the LGDF had the rate been held consistent at 6.47%.

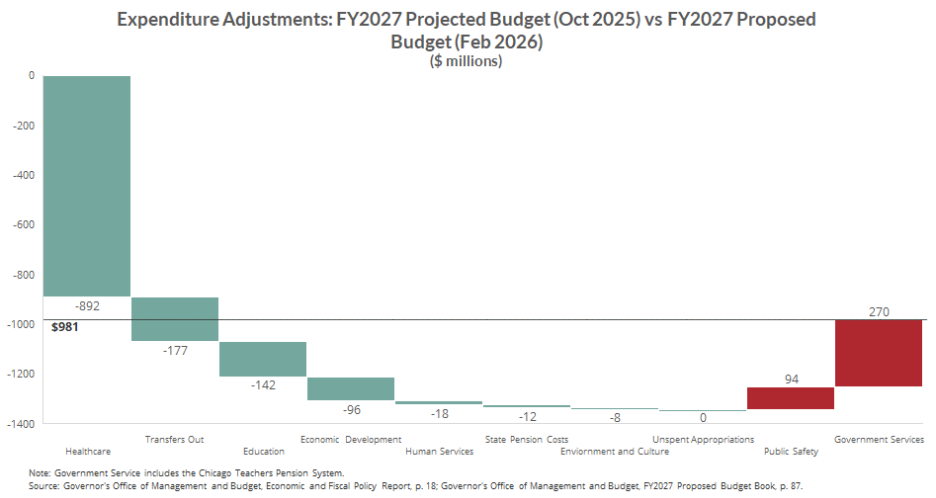

Expenditure Adjustments

As shown in the chart below, the FY2027 proposed budget reflects a downward revision of approximately $981 million in projected spending relative to the October 2025 projections, driven primarily by a $892 million decrease in healthcare spending. Most of this healthcare spending reduction is associated with the State’s medical assistance (Medicaid) program, which is financed through a combination of General Funds, Other State Funds (including provider-related revenues), and federal funds. As noted in the budget, this reflects a reduction in the amount of General Funds allocated to healthcare while increasing the use of special purpose funds. Also, a smaller portion of savings will come from delaying the implementation of certain planned program enhancements, such as behavioral health investments, care coordination programs, and new covered services. As a result, the reduction in General Funds healthcare spending does not necessarily indicate a decrease in overall program funding but rather changes in the financing structure.

Smaller reductions occur across several other areas, including transfers out of the General Fund to other funds ($177 million), education ($142 million), and economic development ($96 million). In comparison, modest increases are proposed in areas such as government services ($270 million) and public safety ($94 million).

Key Takeaways And Themes

The essentially balanced FY2027 proposed budget includes relatively limited spending growth and few major new initiatives compared with the adopted FY2026 budget. Total General Funds revenues increase by about 1.5%, around $827 million, compared to FY2026 revenues, while total spending increases by about 1.6%, or approximately $900 million, reflecting what the administration has described as a “maintenance” budget. The proposal largely maintains existing programs and services, with much of the spending growth—approximately 75% of the increase—driven by statutory and formula-based obligations rather than new initiatives.

These increases include the annual increase in Evidence-Based Funding (EBF) for K–12 education, with the proposed budget providing $305 million in additional funding, compared with $350 million in recent years, as well as required increases in pension contributions (approximately $200 million) and debt service (approximately $79 million). The budget also includes targeted increases for program administration, including support for administering the Supplemental Nutrition Assistance Program (SNAP), reflecting efforts to manage new federal program requirements.

Several themes emerge from the FY2027 budget proposal:

- First, the State relies on incremental budget balancing, closing the projected gap through multiple smaller policy changes and adjustments rather than major tax changes or spending reductions.

- Second, some revenue actions involve timing shifts, particularly the extension of the NOL deduction cap, which increases revenues in the near term while delaying fiscal impacts to future years.

- Third, revenue and spending reallocations across funds play an important role, with adjustments of existing budgetary flows either adding revenues to or decreasing spending from the General Funds.

- Finally, the proposal reflects limited program expansion, with spending largely focused on maintaining existing programs and formula-driven increases rather than introducing significant new initiatives.

Overall, the FY2027 proposal reflects a short-term, maintenance approach that achieves balance in the near term but does not meaningfully address the State’s longer-term structural and fiscal pressures.