February 06, 2013

In this blog, the Civic Federation will explore the City Colleges of Chicago’s fund balance levels as reported in its recently released Comprehensive Annual Financial Report (CAFR) for the fiscal year ending June 30, 2012.

Fund balance is a term commonly used to describe the net assets of a governmental fund and serves as a measure of financial resources. Last year the Civic Federation blogged about changes made to reporting fund balance per the implementation of the Governmental Accounting Standards Board (GASB) Statement No. 54 which reclassifies fund balance components within the governmental funds. The City Colleges of Chicago, however, is not required to implement those changes because, as a public college system with primarily business-type activities, it is not required to report governmental funds.[1] Instead, City Colleges reports net assets for all of its funds.

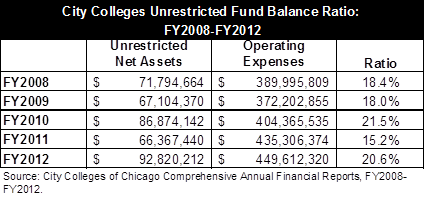

The Government Finance Officers Association (GFOA) recommends that general purpose governments maintain an unrestricted general fund fund balance of no less than two months, or 16.7%, of regular general fund operating revenues or regular general fund operating expenditures. City Colleges is a special purpose, not a general purpose government, but its size and the relative instability of its revenue stream make it prudent for the District to maintain adequate reserves. The GFOA statement adds that each unit of government should adopt a formal policy that considers the unit’s own specific circumstances and that a smaller fund balance ratio may be appropriate for the largest governments. Since the fund balance ratio reflects the savings that a government has accumulated relative to its expenditures for the fiscal year, it is an indicator of the government’s financial ability to maintain current service levels. Data used to calculate the ratio is found in the Statement of Net Assets from the City Colleges audited financial report.

Between FY2008 and FY2012, City Colleges’ general operating funds’ unrestricted net assets increased from 18.4% of operating expenses, or $71.8 million, to 20.6%, or $92.8 million. During this time period, FY2011 is the only year City Colleges dipped below the minimum two months of operating expenses recommended by the GFOA. The healthy level of net assets for City Colleges is a dramatic turnaround from the 1.1% fund balance ratio reported in FY2000.[2]

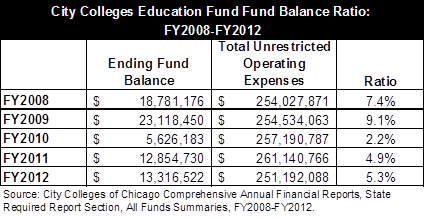

While GASB does not require City Colleges to make financial reports based on governmental funds, City Colleges does include some of this information in the Special Reports section of its CAFR, as required by the State of Illinois. The City Colleges’ Board established a fund balance policy to maintain the fund balance of the Education Fund at a level equal to 3% of unrestricted expenditures.[3] The exhibit below shows the ratio of ending Education Fund fund balance to total unrestricted operating expenses, which includes expenses of the Education Fund, unrestricted Maintenance and Operations Fund and Auxiliary and Enterprise Fund. Only in FY2010 did the District drop below its stated policy.

[1] After issuing Statement No. 34, which created accounting and reporting guidelines for local governments in 1999, GASB issued an amendment to specifically establish standards for public colleges and universities which primarily operate with proprietary funds. For more information, see GASB Statement No. 35.

[2] In FY2000, the District recorded an unreserved fund balance of $3.0 million and operating expenditures of $265.1 million, resulting in a fund balance ratio of 1.1%. See the City Colleges of Chicago FY2000 Financial Statements, p. 3.

[3] City Colleges of Chicago, FY2013 Tentative Annual Operating Budget, p. 9.