September 30, 2010

Citing reliance on one-time revenue sources, such as borrowing, to try and close its FY2011 operating shortfall, Moody’s Investors Service announced last week that it was downgrading its outlook on the State of Illinois’ $25 billion of outstanding General Obligation Bonds (GO Bonds) from stable to negative.

The negative outlook is a warning from the rating agency that if significant steps are not taken to improve the State’s fiscal condition it could face one or more downgrades to its actual rating level. The negative outlook is different from the agency’s negative watch list, which means that definitive action will be taken concerning an issuer’s rating within the next 90 days.

As recently pointed out by the Civic Federation’s Cost of Crisis report, lower credit ratings and negative analysis from investors in the municipal bond markets have led to much higher borrowing costs when the State sells its bonds. The Civic Federation’s analysis of the $9.6 billion in new bonds sold over the last 12 months estimated that Illinois was charged an additional $551.3 million for just one year of borrowing due to downgrades in its credit rating and a poor financial outlook.

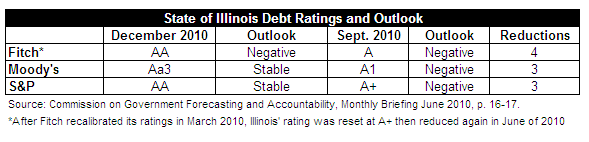

With this latest change from Moody’s, Illinois now has a negative outlook from all three major agencies, including Fitch Ratings and Standard & Poor’s. The following chart shows the rating and outlook from each of the three major agencies in December of 2008 compared to the current level.

Credit ratings are not the only factor that investors consider when determining how much interest to charge and what price to pay for the State’s bonds. Most investors also rely on their own internal analysis of an issuer’s fiscal health before purchasing municipal debt. However, ratings serve as a starting point for market analysis. If the agencies further downgrade Illinois’ credit worthiness, the State can expect to pay more to borrow money in the future.

Although the State has been downgraded multiple times by the rating agencies since December 2008, its debt is still considered investment grade. Fitch and S&P use the same ratings scale starting with AAA as the highest rating and C as the lowest. Both use a plus suffix to indicate higher rated debt within each letter grade, no symbol for the middle and a minus suffix for the lowest. A rating of BB+ is considered speculative grade investment, also known as a junk bond. Illinois would have to be downgraded five times by Fitch and six by S&P to fall to this level.

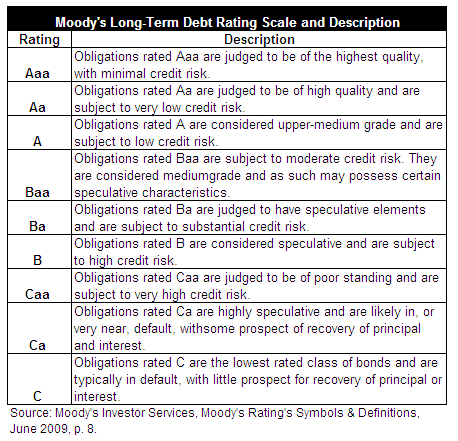

Moody’s maintains a slightly different rating scale than the other two agencies. There are three components of the ratings issued by Moody’s. The first element is the letter grade; Aaa is the highest and C the lowest. The letter grade is then followed by a number 1, 2 or 3 to show what level the debt is within the letter grade, with 1 being the highest and 3 the lowest. Moody’s then assigns an outlook to indicate if the financial condition of the issuer is expected to get better, worse or remain the same. The outlook is denoted by positive, stable or negative. The following chart shows all of the letter grade ratings from Moody’s and the agency’s description of the debt found at each level.

For Illinois long-term debt to show a speculative element and fall below investment grade ratings from Moody’s, it would take six downgrades to Ba1. To be actually judged as fully speculative debt, with a high risk of default, the State would need to be downgraded nine times to B1.

Currently Illinois is tied with California for the lowest ratings of any state from Moody’s and Fitch. S&P rates California slightly lower than Illinois at A-. However, California’s outlook from each agency is currently considered stable.