September 04, 2014

Information included in recent bond disclosures by the State of Illinois indicate that the pension obligation bonds (POBs) sold in 2003 primarily to boost the retirement systems’ assets have earned the minimum investment returns needed to break even in only seven of the last ten years.

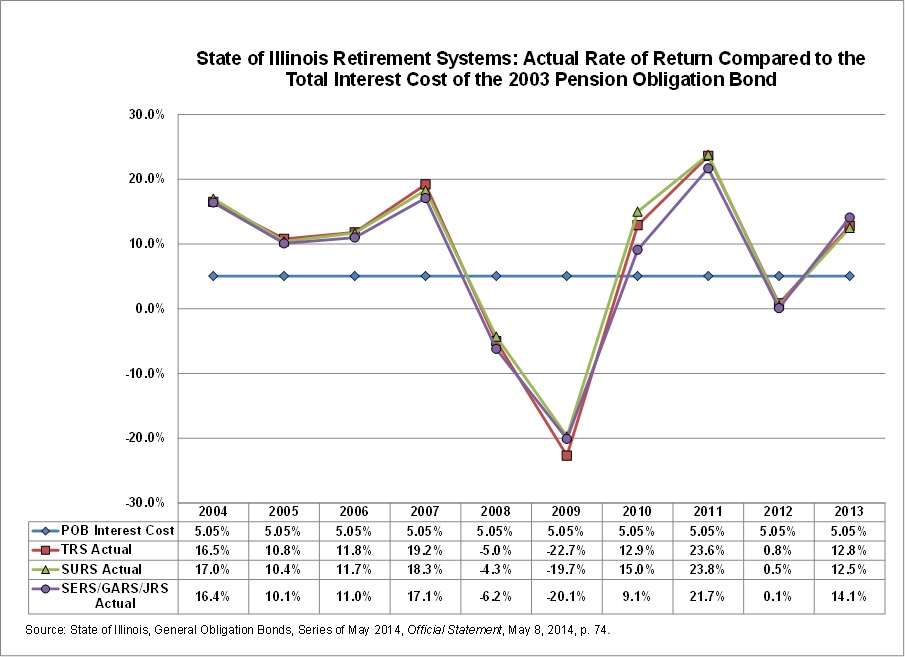

The $10 billion pension bond issuance will cost the State a total of $11.9 billion in interest repaid through FY2033. This amounts to a total interest cost of 5.05%. According to the bond document, any year the retirement systems’ annual rate of return on investments is lower than this amount, the unfunded liabilities of the pension funds increase due to the bond issuance.

The official statement accompanying the State’s $750 million General Obligation bond sale in May 2014 included detailed information regarding investment returns for the State’s five retirement systems. The data show that in 2008, 2009 and 2012 the rate of return was lower than 5.05%.

The following chart compares the actual rate of return on investments to the total interest cost of the 2003 POBs for 2004 through 2013.

When the pension bonds were sold in June 2003, $7.3 billion of the proceeds was deposited into the five State pension funds to increase the retirement systems’ assets. The remainder was used to pay for part of the State’s required FY2003 pension contribution and all of the $1.9 billion contribution in FY2004 that would have otherwise been made using General Funds resources. The State also sold a combined total of $7.2 billion in pension bonds to make its statutorily required contributions in FY2010 and FY2011.

Each year after the State’s retirement systems certify the amount that the State must pay under its statutory funding plan, the law authorizing the 2003 POBs requires the State to reduce its payments by the amount of interest owed on the $7.3 billion deposited into the funds. There is no offset for the FY2010 and FY2011 POBs since all of the proceeds were used for contributions and not to increase the assets above the statutory funding plan.

According to the bond disclosure document, this means that any time the systems annual investment returns exceed the 5.05% interest cost of the bonds the State’s unfunded pension liabilities are lower than they would have been without the additional assets from the pension bond sale. Conversely, any year that the annual investment returns are lower than 5.05%, the unfunded liabilities of the systems are higher than they otherwise would have been (see page 75 and 76 of the official statement for more details).

This interplay between the interest owed on the POBs and the rate of return achieved by the retirement funds defines the risk inherent in borrowing to improve the State’s pension funding and is referred to as interest rate arbitrage. Since Illinois has exceeded this amount in most years, issuing the 2003 POBs at this moment appears have benefited the State financially. At other times the POBs might look less successful if investment returns suffer due to market fluctuations.

A national survey of pension borrowing published by the Center on Retirement Research at Boston College demonstrates the shifting perspective on the success of POB sales to improve pension funding based on market conditions. The study, published in July, reviewed all 5,109 POBs issued across the country by 529 different government entities with a value of $98 billion in 2013 dollars. The researchers concluded that as of 2013 the POBs netted 1.5% in positive earnings. However, the Center’s data show that in 2009 POBs nationally had lost 2.6% in earnings for issuers when the global recession hampered investment returns for pension funds.

The study concludes that since many of the bonds have a 30-year life, a final conclusion cannot be drawn on the overall success of the deals simply from the positive or negative results in any given year.