June 27, 2012

This week the Civic Federation released its annual Status of Local Pension Funding report. This report reviews fiscal year 2010 actuarial valuation reports and financial statements of the retirement funds.[1] The purpose of this report is to compile and analyze basic financial data on ten major local government employee pension funds in the Chicago area.[2] It is intended to provide policymakers, pension trustees, pension fund members and taxpayers with information they need to make informed decisions regarding public employee retirement benefits. It explains common indicators of pension fund fiscal health and causes for change in the health of the local funds.

The following pension funds are included in the analysis.

- Municipal Employees’ Annuity and Benefit Fund of Chicago3

- Laborers’ and Retirement Board Employees’ Annuity and Benefit Fund of Chicago3

- Firemen’s Annuity and Benefit Fund of Chicago3

- Policemen’s Annuity and Benefit Fund of Chicago[3]

- County Employees’ and Officers’ Annuity and Benefit Fund of Cook County4

- Forest Preserve District Employees’ Annuity and Benefit Fund of Cook County[4]

- Metropolitan Water Reclamation District Retirement Fund

- Retirement Plan for Chicago Transit Authority Employees

- Public School Teachers’ Pension and Retirement Fund of Chicago[5]

- Park Employees’ & Retirement Board Employees’ Annuity and Benefit Fund[6]

Highlights of the data compiled on the ten pension funds are summarized below.

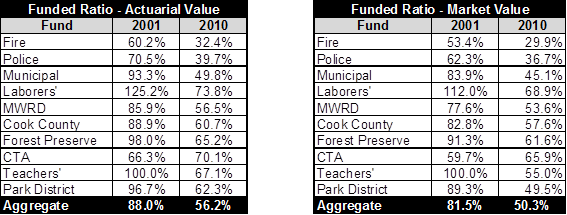

Funded Ratios:[7] The actuarial value funded ratio of each fund fell in FY2010 from FY2009.[8] All ten funds now have actuarial value funded ratios under 75%, ranging from a low of 32.4% for the Fire Fund to a high of 73.8% for the Laborers’ Fund. The actuarial value funded ratio for the aggregate of all ten funds’ assets and liabilities was 56.2% in FY2010, down from 88.0% in FY2001. Market value funded ratios were considerably lower, at an aggregate ratio of 50.3% in FY2010.[9] The lowest market value funded ratio was the Fire Fund at 29.9%, and the highest was the Laborers’ Fund at 68.9%.

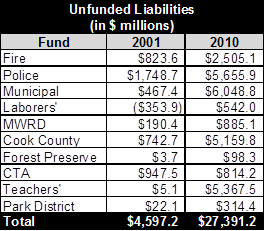

Unfunded Liabilities:[10] Between FY2001 and FY2010 the aggregate unfunded actuarial accrued liabilities for the ten funds increased by $22.8 billion, rising from $4.6 billion to $27.4 billion. Unfunded liabilities per capita in Chicago for the ten local funds rose from $1,189 in FY2000 to $8,993 in FY2010. For the four City of Chicago pension funds alone, FY2010 unfunded liabilities were $14.8 billion, or $5,473 per capita.

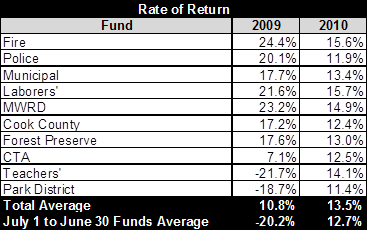

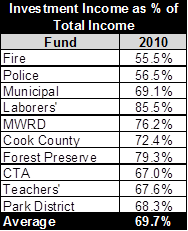

Investment Income and Rate of Return:[11] The average rate of return on pension plan assets for funds with a January 1 to December 31 fiscal year was 13.7% in FY2010, down from 18.6% in FY2009. The average rate of return for funds using a July 1 to June 30 fiscal year was 12.7% in FY2010, up from -20.2% in FY2009. Investment income represented between 56% and 86% of total FY2010 income.

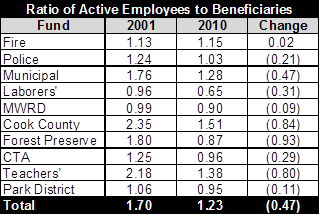

Ratio of Active Employees to Beneficiaries: Between FY2001 and FY2010 the ratio of total active employees to beneficiaries for the ten funds combined has gradually dropped from 1.70 actives per beneficiary to 1.23, indicating that there are fewer active employees supporting more retirees. The Laborers’, MWRD, Forest Preserve, CTA and Park District Funds all had more beneficiaries than actives in FY2010.

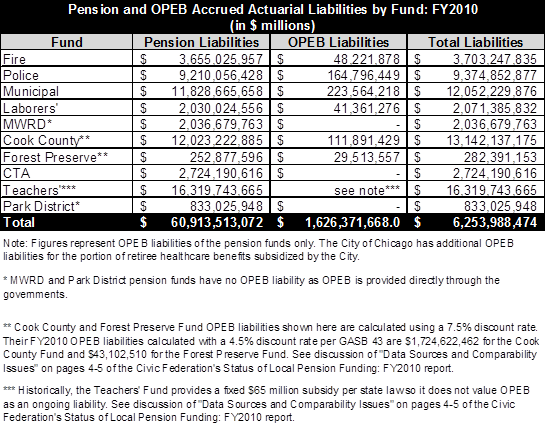

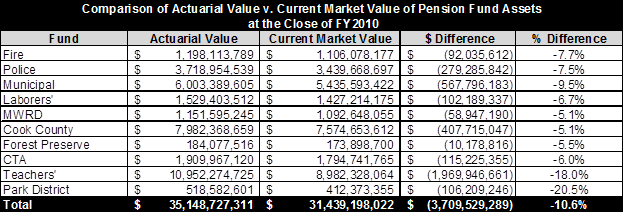

Assets and Liabilities: The ten pension funds had approximately $62.5 billion in combined pension and Other Post Employment Benefit (OPEB) accrued liabilities for FY2010.[12] Pension liabilities for the funds totaled $60.9 billion and OPEB liabilities of the funds totaled $1.6 billion. The funds’ assets had an aggregate actuarial value of $35.1 billion and a market value of $31.4 billion.

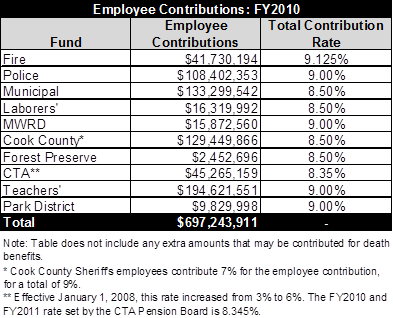

Employee Contributions: For all ten funds, employee contributions totaled $697.2 million in FY2010. Most employees contribute at rates ranging from 8.5% to 9.125% of salary.[13]

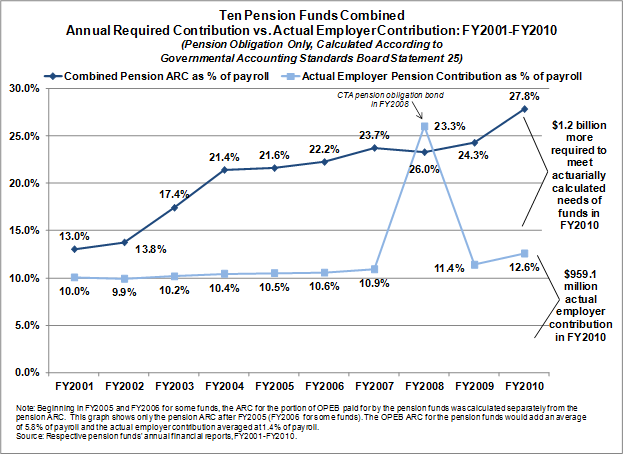

Employer Contributions and ARC: All funds received their statutorily required employer contributions in FY2010. However, none of the employers contributed the full actuarially calculated annual required employer contribution (ARC) in FY2010 and only two funds, the Teachers’ Fund and the CTA Fund, contributed more than 50% of the pension ARC.[14] In the aggregate, in order to meet the pension ARC in FY2010, employers should have contributed $2.1 billion. Instead they contributed less than half that amount, $959.1 million, falling short by approximately $1.2 billion. Employers contributed an aggregate equivalent of 12.6% of payroll to the pension funds for pension obligations, but in order to meet the ARC, they should have contributed an additional 15.2% for a total of 27.8% of payroll in FY2010.

For more detailed information on the status of local pensions, read the full report here.

[1] Fiscal year 2010 data is the most recent audited data available for all ten pension funds.

[2] In this report the terms “pension fund” and “pension plan” are used interchangeably. The term “local government” is used here broadly and includes the Chicago Transit Authority, an Illinois municipal corporation. The seven governments and ten funds analyzed in this report were created by Acts of the Illinois General Assembly.

[3] The City of Chicago enrolls its employees in four different pension systems.

[4] The funds of Cook County and the Cook County Forest Preserve District are governed by the same pension board.

[5]Certified Teachers employed by the Chicago Board of Education participate in the Public School Teachers’ Pension and Retirement Fund of Chicago. Most other employees of the Board of Education are enrolled in the City of Chicago’s Municipal Employees’ Annuity and Benefit Fund. Approximately 16,061, or 52.3%, of Municipal Fund members considered to be active by the Fund are Board of Education employees. Chicago Public Schools, Comprehensive Annual Financial Report for the fiscal year ended June 30, 2011, p. 75. A very small number of Board of Education employees are enrolled in the Laborers’ Fund.

[6]The fiscal year of the Park Employees’ and the Public School Teachers’ pension funds is July 1-June 30. The other eight funds use a January 1 – December 31 fiscal year. On May 31, 2012, the Illinois General Assembly passed Senate Bill 3629, which, if signed into law, would amend the Park District Fund’s fiscal year to be concurrent with the calendar year and the sponsoring government’s fiscal year, beginning January 1, 2013.

[7] Funded ratio is the ratio of assets to liabilities. Usually this ratio is expressed in terms of actuarial values, as required by GASB 25. When a pension fund has enough assets to cover all its accrued liabilities, it is considered 100% funded.

[8] Actuarial value of assets smoothes asset gains and losses over four or five years.

[9] Market value of assets can be reported by their market value, which recognizes unrealized gains and losses immediately in the current year and can produce significant fluctuation year-to-year. This measure is subject to volatility in the market.

[10] Unfunded liabilities are the current liabilities not covered by actuarial assets. It is calculated by subtracting the actuarial value of assets from the actuarial accrued liability of a fund.

[11] The Civic Federation calculates investment rate of return using the following formula for all funds: Current Year Rate of Return = Current Year Gross Investment Income/ (0.5*(Previous Year Market Value of Assets + Current Year Market Value of Assets – Current Year Gross Investment Income)). This is not necessarily the formula used by all funds’ actuaries and investment managers, thus investment rates of return reported here may differ from those reported in a fund’s actuarial statements. However, it is a standard actuarial formula.

[12] This report focuses only on OPEB obligations for the employees of the sponsoring government, not the fund staff. The obligation for fund staff is typically very small compared to the obligation for government employee fund members.

[13] In FY2009, CTA employees paid 6.0% of salary, but this increased to 8.345% in FY2010. CTA is the only government reviewed in this report whose employees also participate in Social Security.

[14] ARC is an accounting reporting requirement, not a funding requirement. However, it does represent a reasonable calculation of the amount of money the employer might contribute each year in order to cover costs attributable to the current year and to reduce unfunded liabilities.